Intraday trading in stock options looks glamorous from the outside, but the real edge comes from brutal honesty with data and the courage to refine a system step by step. Over the last month, a new basket of stock‑options strategies has been quietly doing exactly that in paper trading on Tradetron with a capital of ₹2 lakh per strategy. The early numbers are not just encouraging; they open up an important question every intraday trader must finally answer with evidence, not theory: should there be an overall portfolio stop loss?

The journey so far

These strategies were first deployed on 11 December 2025, focusing on buying stock options with leg‑wise stop losses for each stock. For ten consecutive trading sessions, they have been consistently hitting their intraday targets, which naturally builds confidence but also demands a deeper risk‑management framework.

The stop loss dilemma

From day one of intraday training, one lesson was clear: there is no certainty in the market, only probabilities. That is why leg‑wise stop losses were part of the design from the beginning, protecting each option position independently. Yet, until now, there was no overall SL for the combined strategy, meaning a sequence of losing trades on a volatile day could, in theory, create a deeper‑than‑necessary drawdown. The natural question arises: is a portfolio‑level stop loss good or bad for a system that is already performing well?

Turning theory into data

Rather than debating the answer in theory, the decision was made to let data speak over the next month. Multiple versions of the strategy have now been created with different overall stop losses: ₹1,000, ₹2,000, ₹3,000 and so on, all the way up to ₹10,000. Each variant will run in parallel on Tradetron, using the same underlying logic but with a different cap on maximum daily loss. At the end of the month, there will be a clear picture of how overall SL levels affect total returns, maximum single‑day loss, and the smoothness of the equity curve. The variant that offers the best balance of return and drawdown—not just the highest raw profit—will be the one chosen for live deployment.

Fixing live‑trading obstacles

This current phase is not just about SL experimentation; it is also the result of solving two practical obstacles faced during early live trading tests in stock options. The first issue was data‑feed related: sometimes the underlying moved, but the option LTP did not update as expected, causing stop losses to be skipped or entries to mis‑align. The solution was simple but powerful—make the entry condition depend on the option price itself, not just the underlying. If the option is not moving, there is no trade; if there is a trade, the option price is definitely live, so stops and targets behave as designed.

The second hurdle was the imbalance between entries and repairs. Initially, the system could generate many entries but only a single repair, which meant that when the market gave fresh opportunities, the strategy could not fully participate. On one such day, this limitation translated into a painful missed profit. That limitation has now been removed by configuring multiple repairs—“as many repairs as entries”—so the strategy can actively manage positions throughout the day instead of firing once and staying passive.

Why these screenshots matter

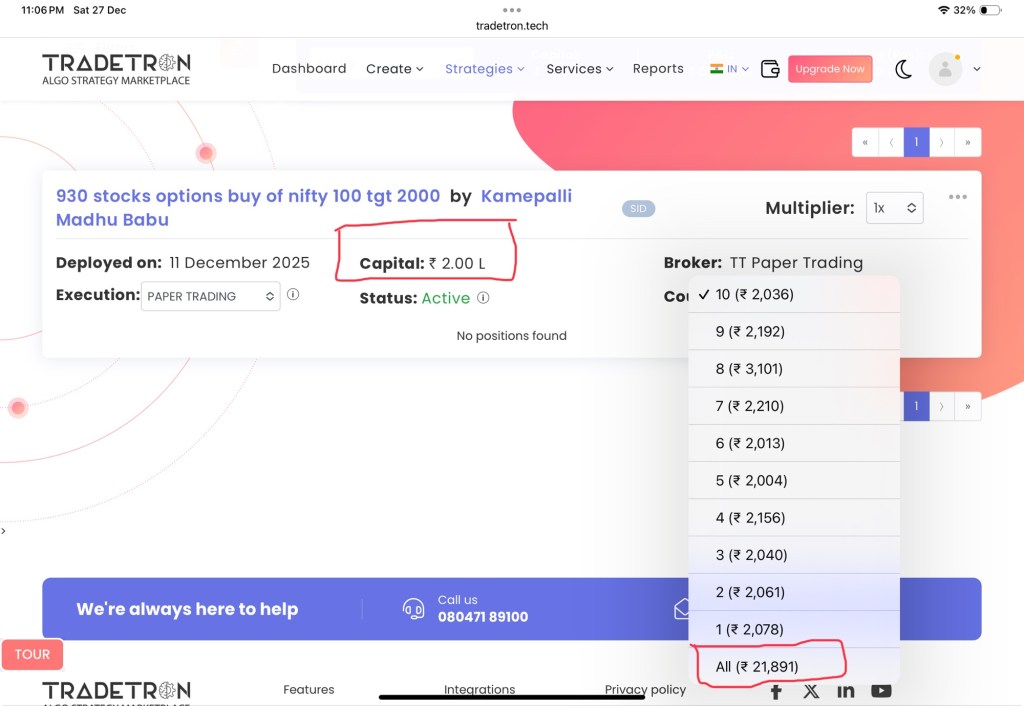

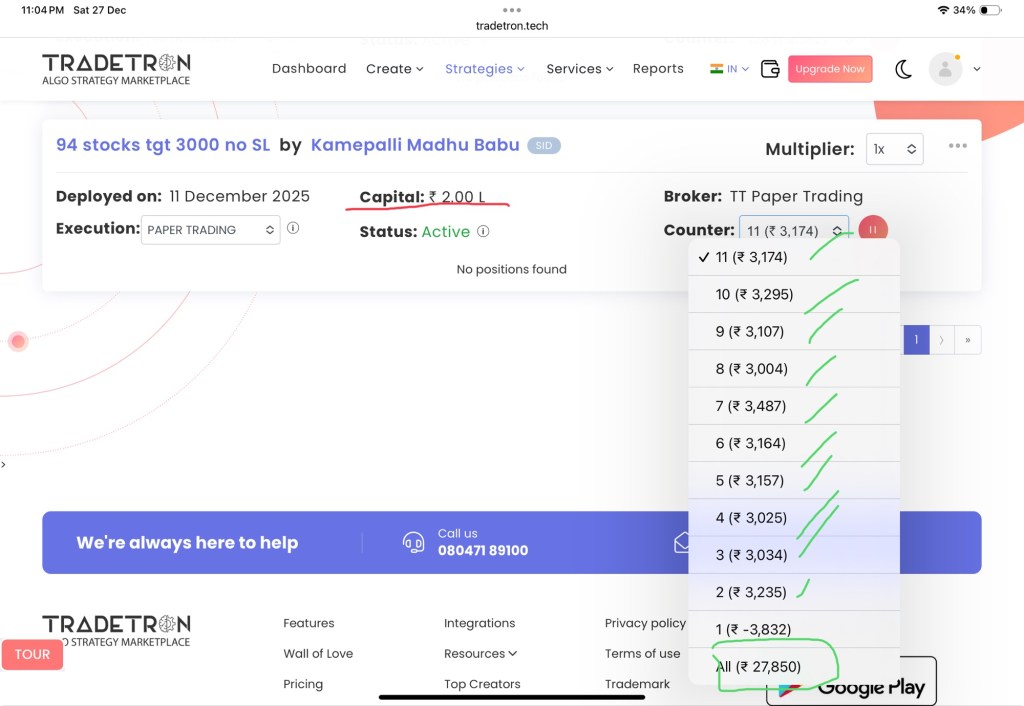

The attached screenshots capture this evolution in numbers. The first shows the “930 stocks options buy of nifty 100 tgt 2000” strategy with a capital of ₹2 lakh and an overall P&L of around ₹21,891 across counters, a strong start for a system in testing. The second screenshot shows another variant, “94 stocks tgt 3000 no SL,” again allocated ₹2 lakh, already sitting on a larger cumulative profit of approximately ₹27,850 with multiple profitable counters marked. These images are not just proof of concept; they are the baseline against which the new SL‑based variants will be judged.

Looking ahead

The next thirty days will decide whether the hero remains the “no overall SL” version or whether one of the carefully chosen daily stop bands emerges as the more robust long‑term player. Whatever the outcome, the philosophy is clear: logic and theory are useful, but capital will ultimately follow the variant that proves itself in hard data. With leg‑wise SLs refined, option‑price‑based entries in place, and repair‑continuous logic fully aligned with the number of entries, these stock‑options strategies are now positioned to become genuine game‑changers in the intraday space.

Leave a comment