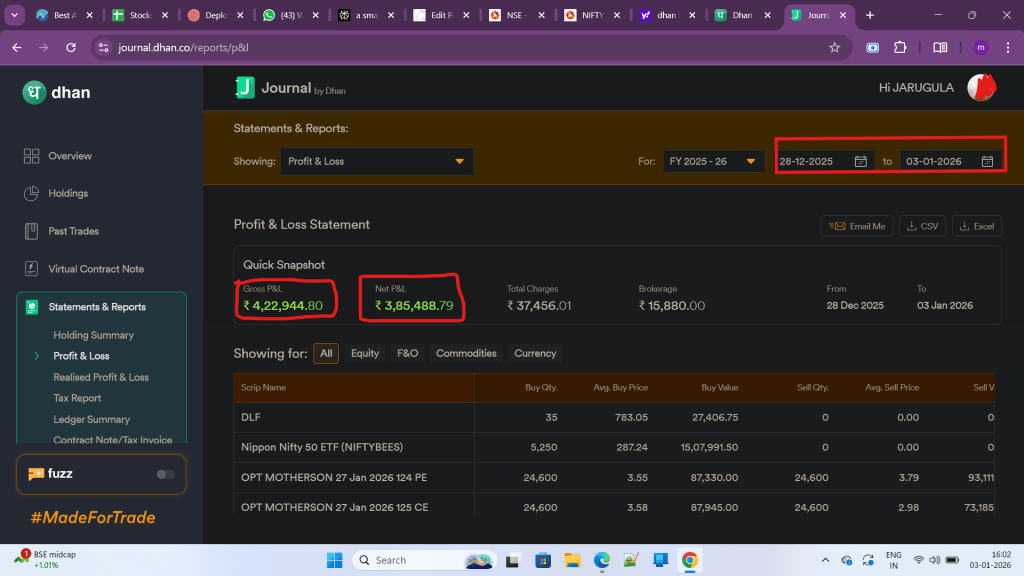

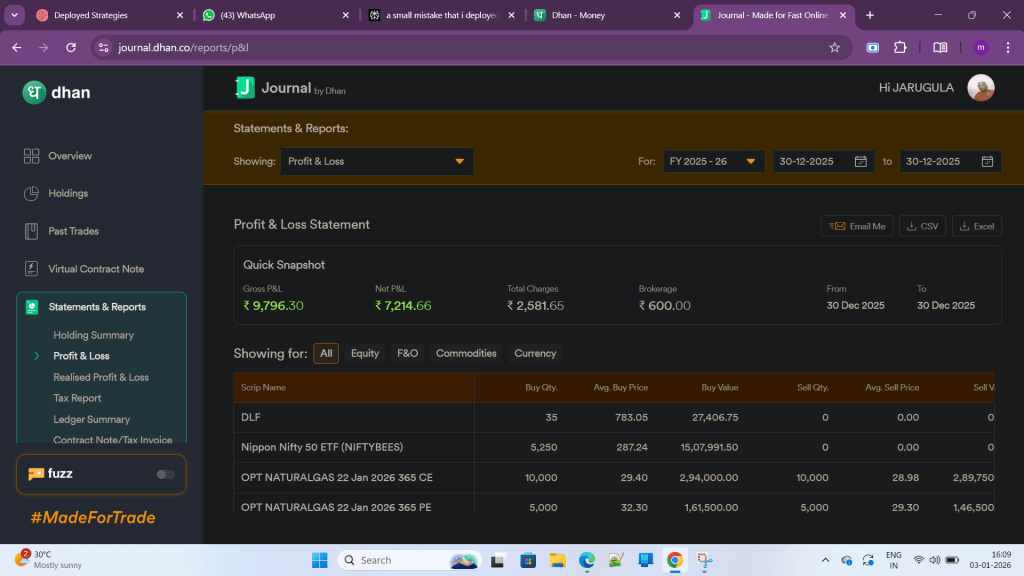

A Strong Week, But Not “Unlimited Joy”

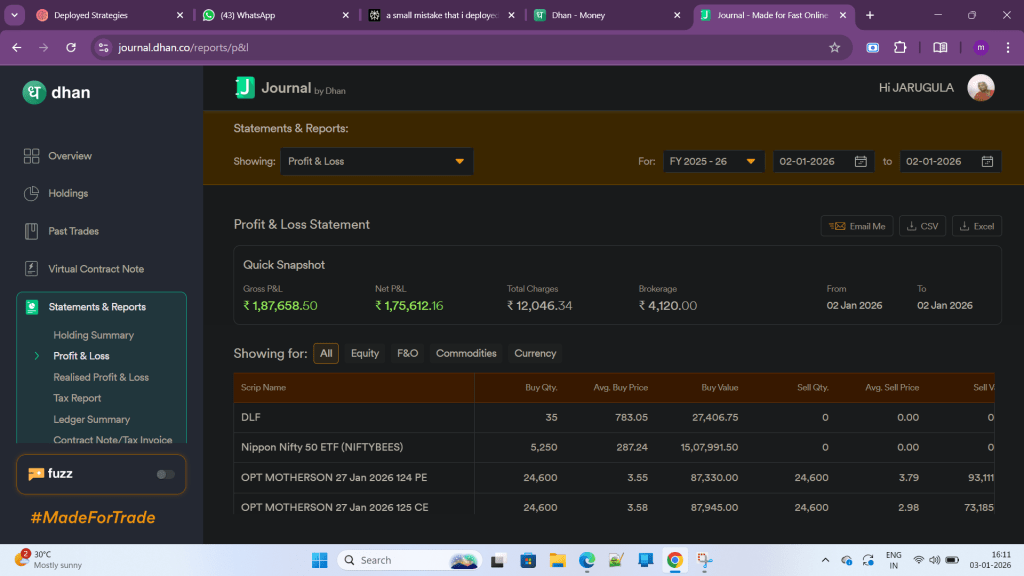

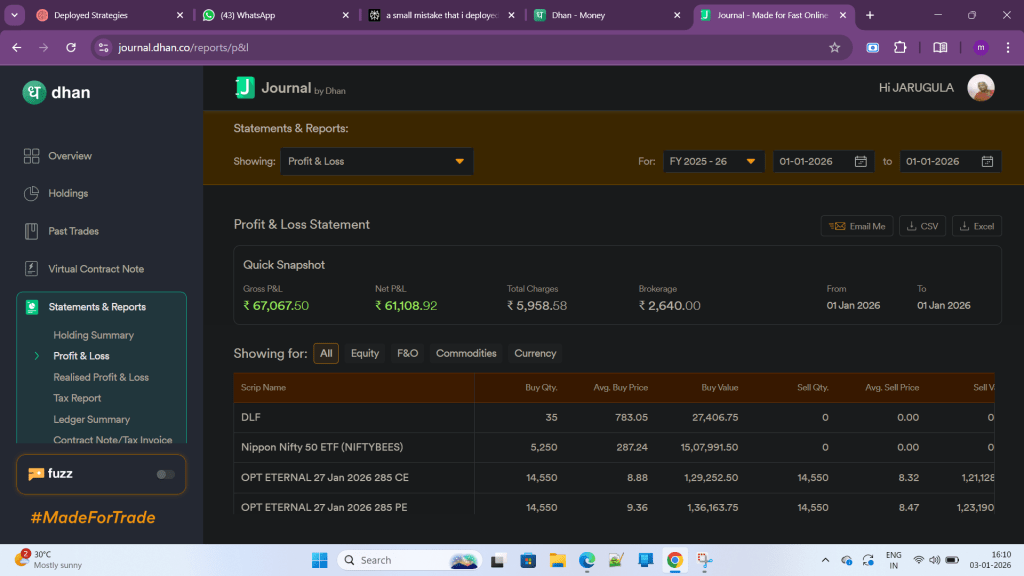

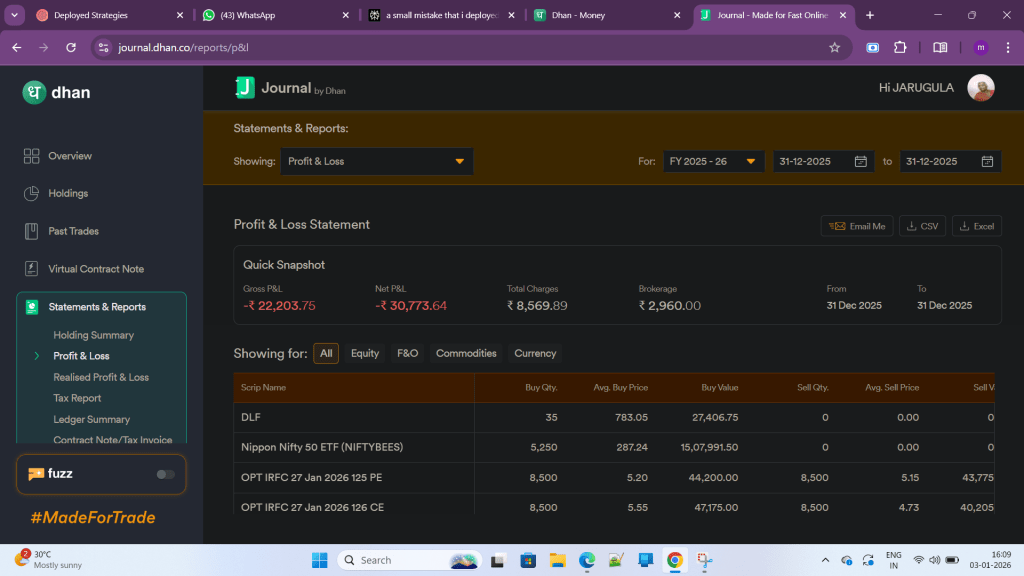

Last week’s numbers were impressive: multiple days of solid green, with only Tuesday left on the table because fresh stock-option positions were not allowed on monthly expiry day due to physical settlement rules. On the first three days, only 3 lots per stock were deployed, and on the last two days, the exposure was scaled up to 6 lots, which naturally amplified the absolute profits.

Yet this is not the time for unlimited celebration. It is just one phase in a normal market cycle where strong trending weeks and dull, directionless weeks keep rotating. Treating a good week as “normal business” rather than a jackpot keeps a trader grounded and protects against overconfidence.

On Tuesday, the strategy signalled trades, and forward testing also showed strong potential performance, but the exchange’s restriction on fresh stock-option positions on monthly expiry day meant no new trades could be taken. The system did its job in forward testing (paper trading) well.

This is an important psychological reminder. Some missed profits are not “mistakes” but structural constraints of the derivatives market, especially around physical-settlement expiries, and accepting that calmly is part of being a professional trader.

Lots, Risk, And Normalizing Big Numbers

Deploying 3 lots initially and then 6 lots later in the week was a deliberate way to scale risk as confidence in live behaviour increased. The higher lot size naturally made the last two days look spectacular on the statement, but in reality it was the same underlying edge with a slightly larger position.

Professional trading means normalizing big P&L numbers emotionally. Profits should change the equity curve, not the trader’s character; the real metric is how faithfully the plan was executed at each lot size.

Targets Versus Open-Ended Profits

Last week also highlighted a deeper structural choice: comfort versus returns. Some strategies were run with fixed profit targets of 2,000–3,000, and these targets were hit reliably, giving psychological comfort and quick closure. However, those same targets also capped “bomblastic” moves where the market kept trending, and the system would have delivered far larger profits without a hard cap.

In parallel, a set of target‑less strategies was running, allowing profits to trail and breathe, and these captured a much bigger portion of large moves, at the cost of enduring more open fluctuation. This side‑by‑side experience made one truth crystal clear: if the goal is long‑run capital growth, open‑ended exits with intelligent risk management beat small, comfortable caps.

Trading literature has always emphasised letting winners run and avoiding premature profit booking, and many classic strategy authors advocate exits that maximise expectancy rather than emotional relief. But real conviction in that idea only comes when a trader sees, in personal forward testing, how much upside is left on the table by rigid profit targets.

That is why the next phase is clear: target‑based variants will be kept only in forward testing or paper trading, while live capital will increasingly be allocated to robust, well-tested strategies without hard profit caps, supported by disciplined position sizing and risk controls. The mission now is simple: — to keep sieving through every statistic, every weekend, until the portfolio is dominated by strategies that may not feel the most comfortable in the moment but deliver superior returns over the long run.

Leave a comment