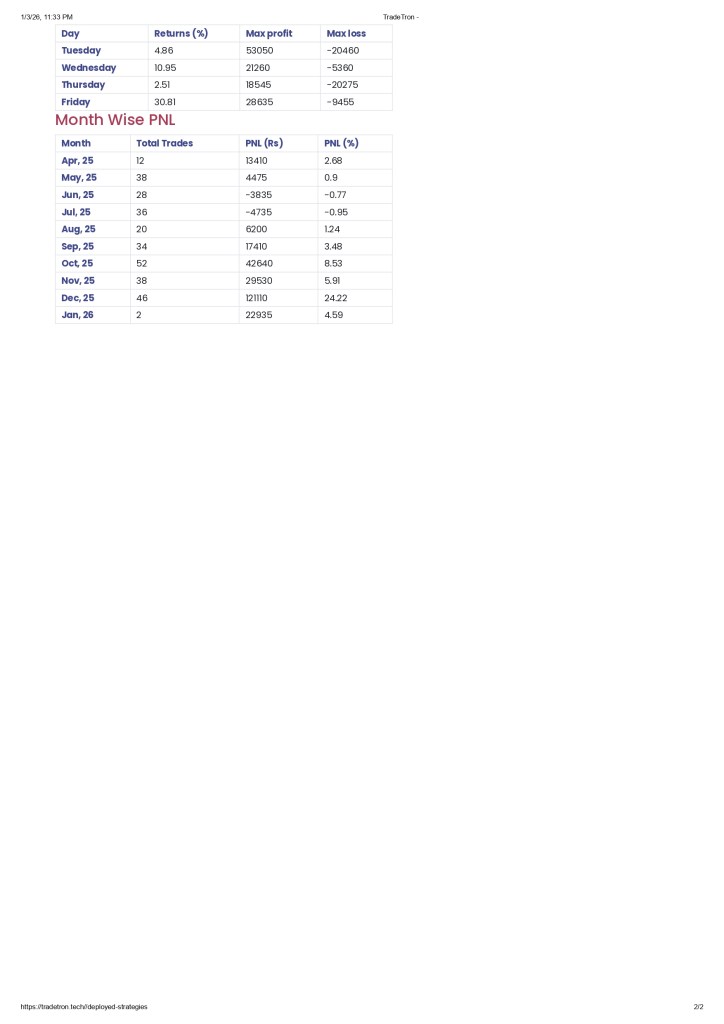

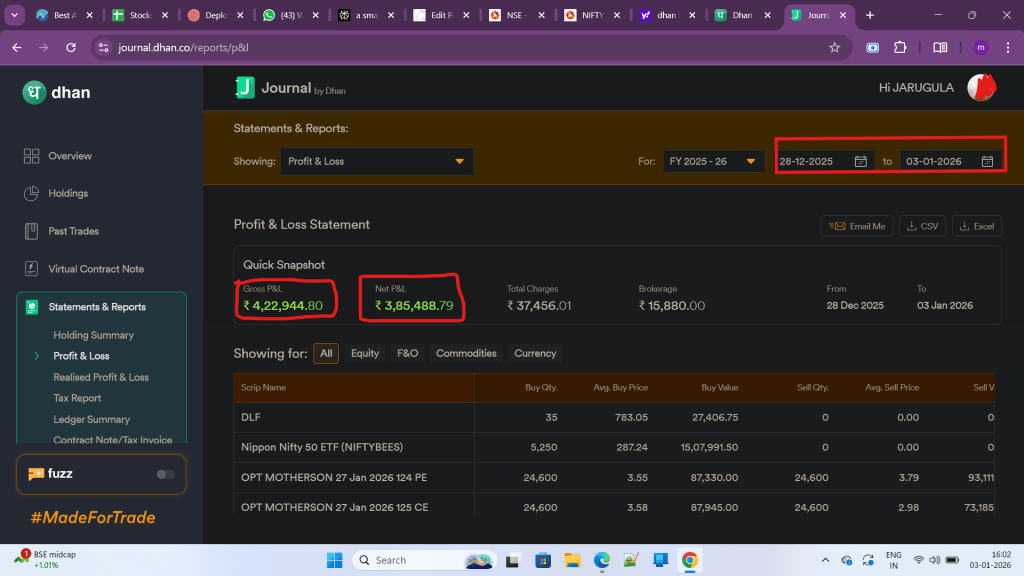

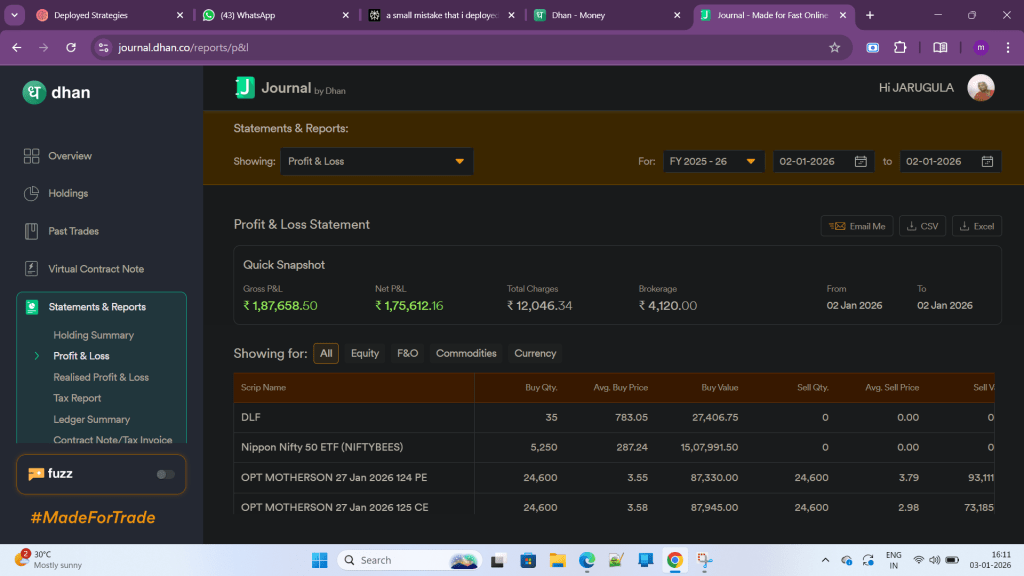

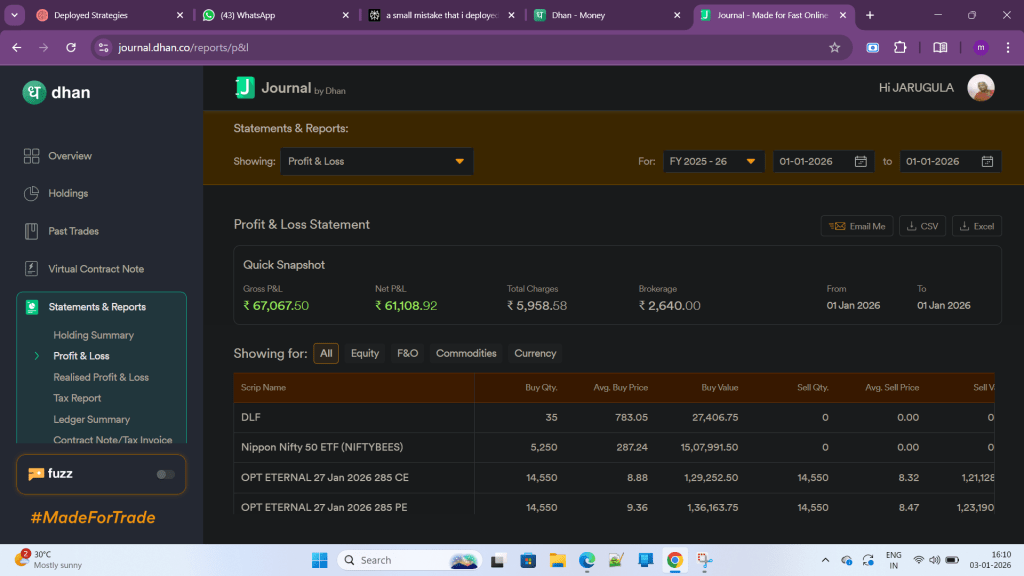

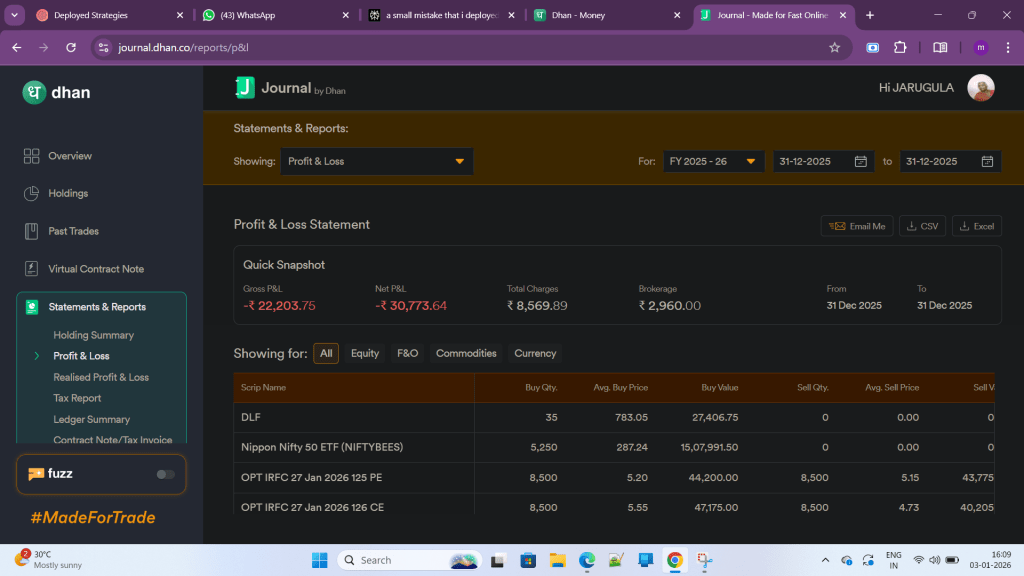

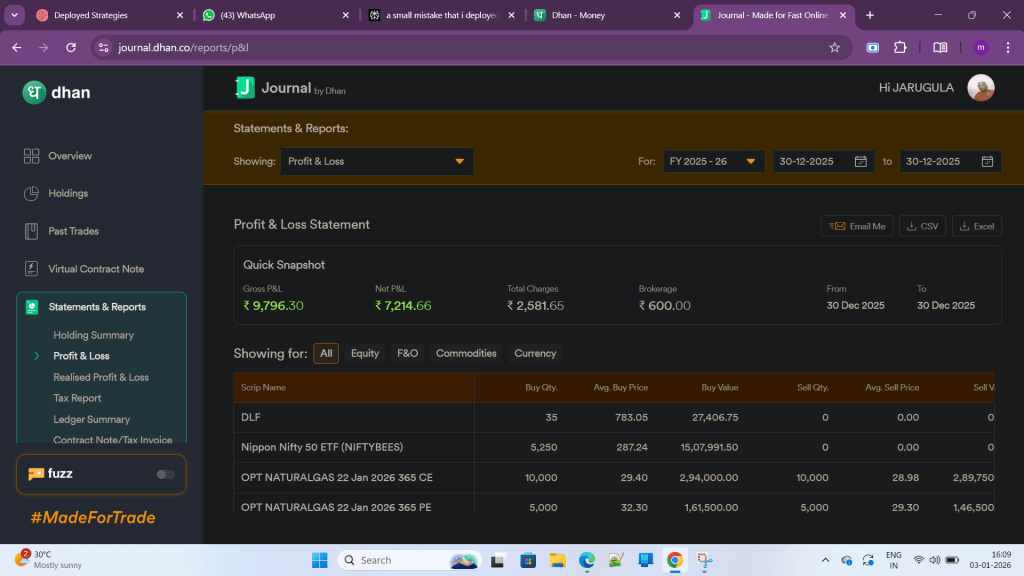

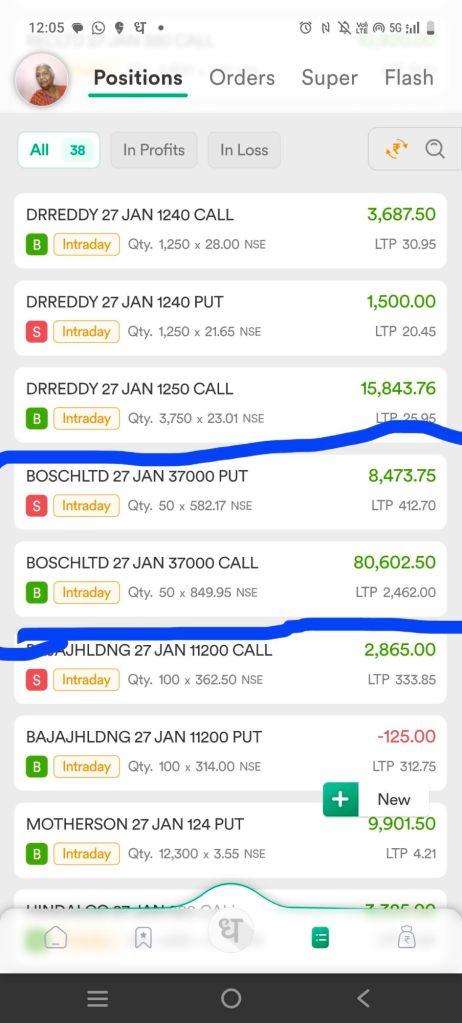

Next week marks a strategic deployment in live algo trading with heavy diversification across natural gas options (14 lots), crude oil options (8 lots), silver futures (2 lots), Nifty index options (7 lots), and stock options (69 lots) across 10 to 14 stocks. Review happens next Saturday to assess profits and losses, but decisions stay data-driven over long-term performance, not weekly swings . Fixed ₹2000-₹3000 target strategies pause in live after booking targets last week but missing bigger gains; forward testing continues with varied SLs and targets .

Deployment Breakdown

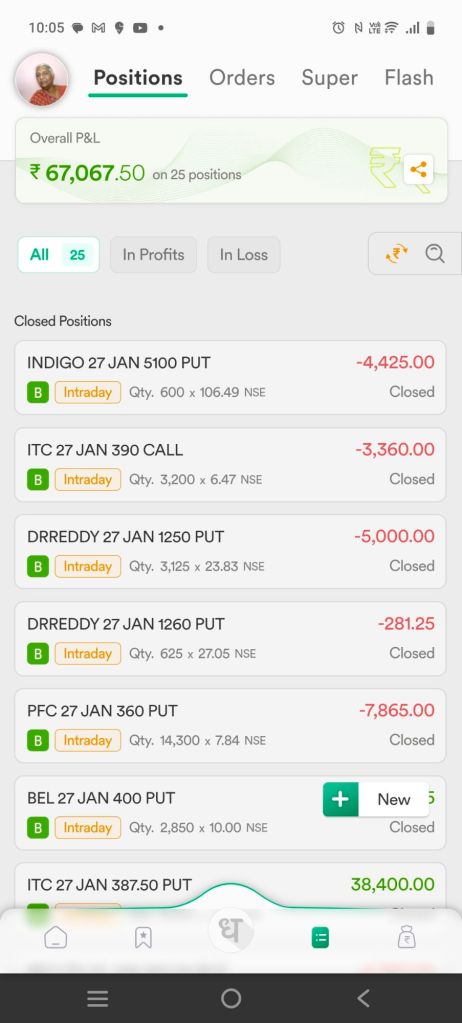

Positions span MCX commodities and NSE derivatives for balanced exposure.

This mix reduces correlation risks from past drawdowns in single assets like Nifty and natural gas .

Forward Testing Fixed Targets

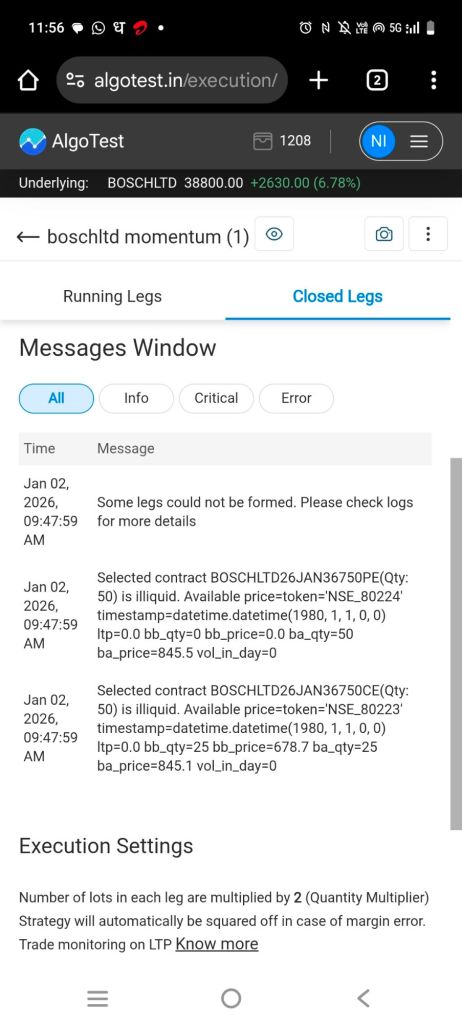

Strategies hitting ₹2000-₹3000 daily stay in sandbox mode only, observing SL adjustments post-last week’s live. Live capital flows to uncapped versions for full trend capture, aligning with 5+ years of refining data-backed systems . Review post-next week decides scaling, prioritizing equity curves over short bursts .

Embracing Profits and Losses Alike

Humongous profit weeks excite sharing; loss weeks less so, but both fuel the business—I believe that losses are as controlled “expenditures” like buying raw materials before profits roll in . controlled losses build resilience for asymmetric wins in algo trading .every one may not share same beliefs about losses this may not be comfortable me sharing them. That’s why generally I avoid sharing losses. But I must accept proudly that I do book losses but controlled losses

Past performance does not guarantee future results. Derivatives trading carries substantial risk of capital loss due to volatility, slippage, and margins. Deploy only risk capital , test in paper mode, and consult SEBI-registered advisors. Not investment advice—trade responsibly.