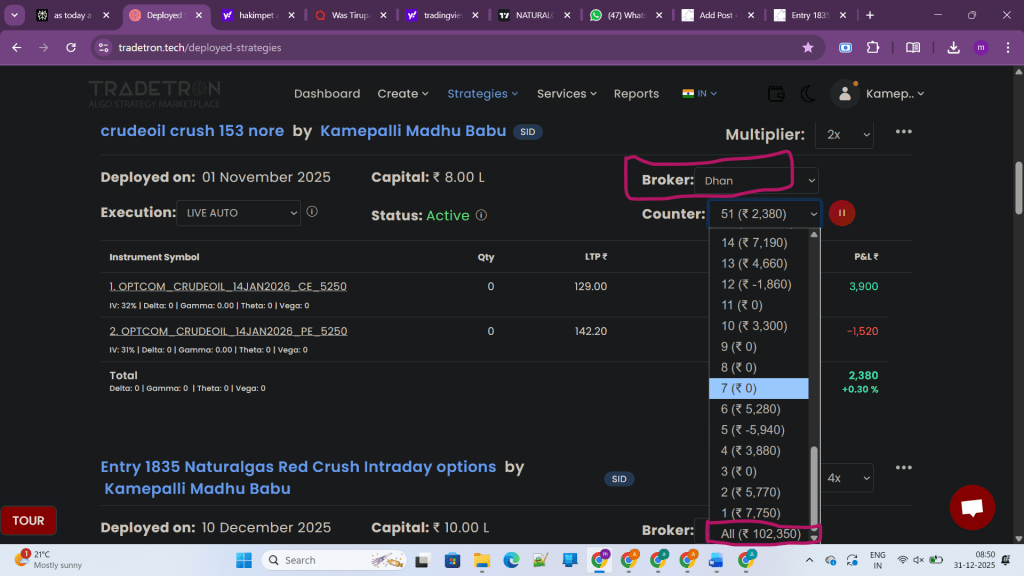

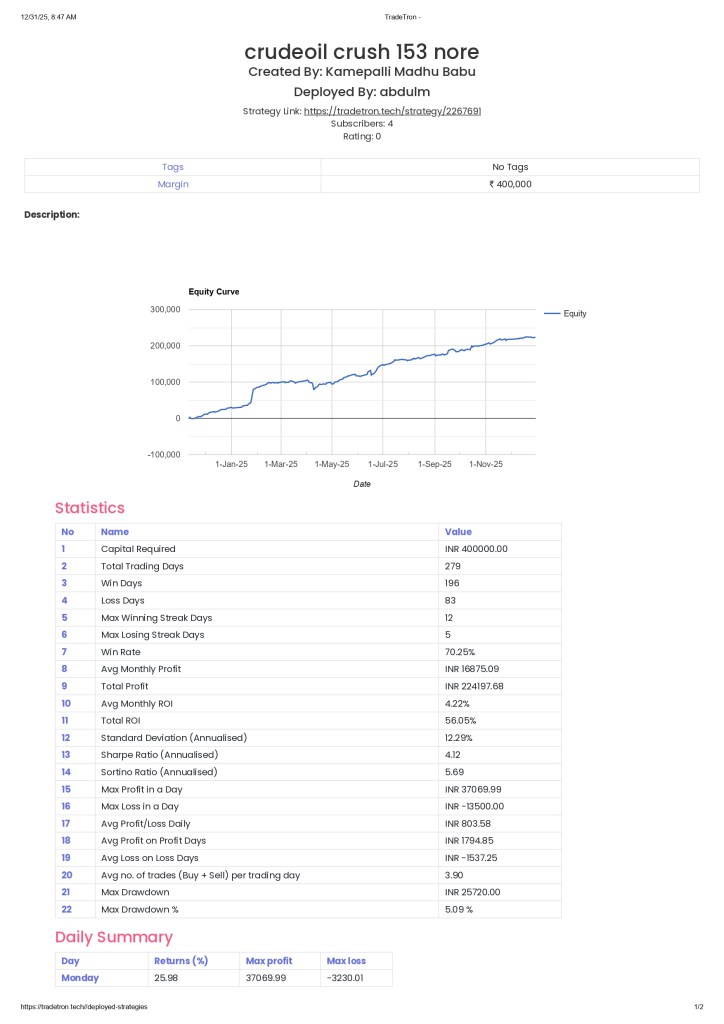

Crude Crush 1530 stands as the most reliable strategy in live deployment over the past year on Tradetron with Dhan broker, crossing ₹1 lakh in profits as of December 31, 2025. This intraday crude oil options system targets MCX evening volatility, delivering consistent execution in real-market conditions.

Deployed continuously for 12 months, Crude Crush 1530 has generated over ₹2,27,000 in verified profits, showcasing resilience across crude oil’s volatile swings. The dashboard reveals multiple successful legs with positive P&L on key dates like November and December 2025, confirming real-time profitability beyond paper trading(Forward Testing). Evening session focus aligns with peak MCX liquidity from 3:30 PM to 11:30 PM, where global crude moves create premium opportunities.

This intraday options approach enters crude oil positions post-1530 IST, capitalizing on US session overlap for momentum and mean-reversion setups. Automated via Tradetron-Dhan integration, it handles multi-leg executions (e.g., 2-4 lots) with Dhan’s multiplier. Risk controls include time-based exits before session close, avoiding overnight gaps from EIA reports or OPEC news.

Crude oil’s high volatility suits this system’s premium capture, outperforming in range-bound and breakout regimes common to MCX evenings. Live stats show strong win rates on deployed legs, with Dhan enabling efficient collateral use.

Full Tradetron automation removes emotional bias, with Dhan’s free APIs handling live execution seamlessly for MCX options. Strategy suits working professionals targeting evening crude moves, backed by one-year empirical data over diverse market conditions.

Past performance does not guarantee future results. This strategy faced drawdowns and will encounter losing periods; crude oil volatility can spike unexpectedly from geopolitical events, inventory data, or USDINR shifts. Trading derivatives involves substantial risk of capital loss; slippage, broker issues, and margin calls can erode profits. Not investment advice—consult a SEBI-registered advisor, trade only risk capital, and review all risk disclosures before deployment.

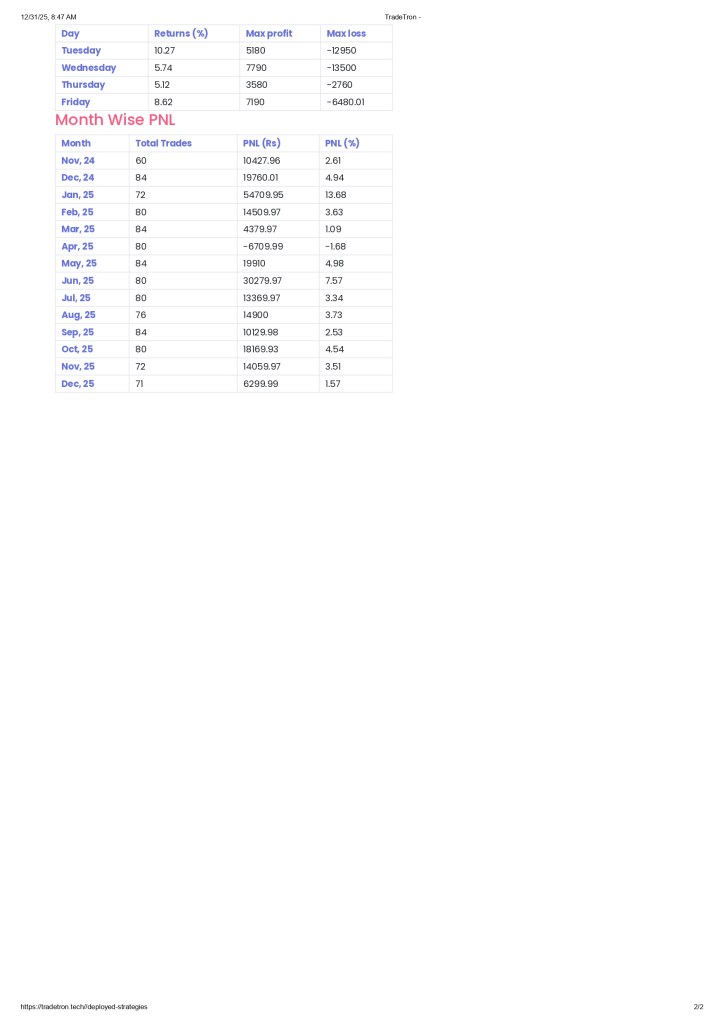

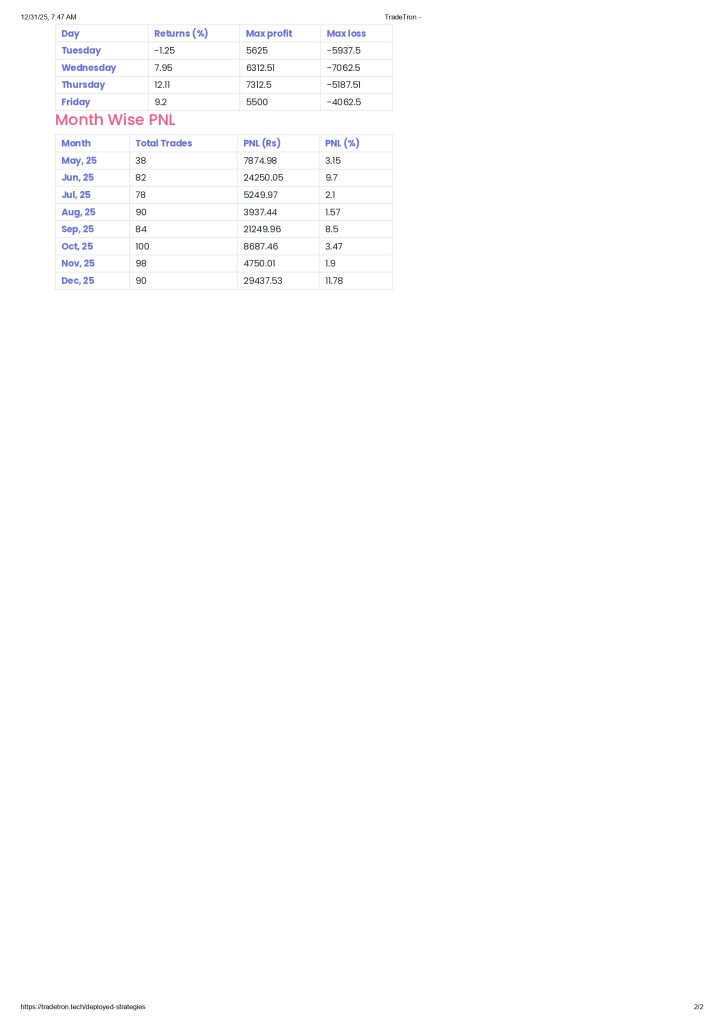

Entry 1835 Naturalgas Red Crush Intraday Options has delivered more than 60% win rate and over 5% monthly returns in the evening session since May, making it a compelling MCX options strategy for systematic traders. Yet every trader must remember that these outcomes are historical; past returns do not guarantee future performance, and capital is always at risk.

This strategy trades natural gas options on MCX, targeting the evening session when liquidity and volatility typically rise. Natural gas’s intraday swings create opportunity for premium capture and quick risk adjustments.

Backtests and live deployment data since May show a win ratio comfortably above 60%, giving traders a statistical edge over pure directional guessing. On a portfolio basis, the strategy has produced more than 5% average monthly returns, which is strong for a collateral-efficient intraday system. However, these numbers are period-specific and may compress sharply during adverse time of this strategy.

Positions are initiated only in the evening segment, avoiding daytime noise and targeting well-defined volatility pockets. The intraday framework ensures positions are squared off before the session ends, limiting overnight gap risk from global commodities or macro news. Position sizing is calibrated to an indicative capital requirement of about ₹2.5 lakh, with risk managed through pre-defined exits and time-based closures.

The strategy is available on Tradetron, allowing full automation with connected brokers and removing execution emotion from the decision loop. Deployment is subscription-based, with a transparent monthly fee structure so traders can factor cost into expected net returns. Cloud execution, reporting, and broker integrations make it accessible even for traders who do not code.[2]

Despite strong recent performance, this strategy can and will face losing streaks, drawdowns, and regime shifts in natural gas volatility. Slippage, broker/API failures, and sudden margin changes can also materially affect actual results versus Paper Trading (forward testing). This article is for educational purposes only and is not investment advice; derivatives trading involves substantial risk of loss, and past performance does not guarantee future returns under any circumstances.

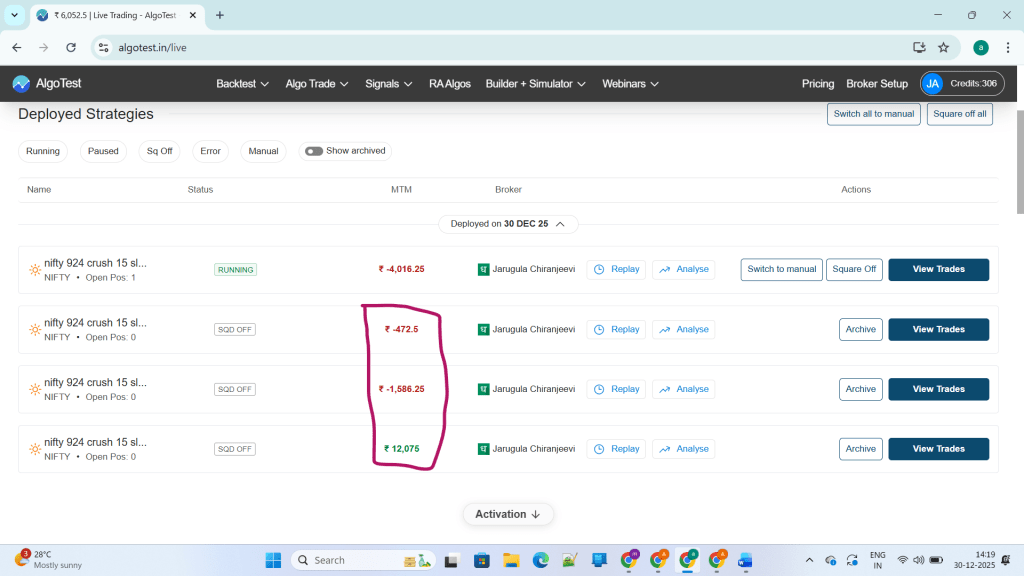

Dhan’s pledged collateral unavailability strikes again on critical trading days, frustrating algo traders despite a year of otherwise smooth operations. This marks the third such incident in 12 months, pushing consideration of a Zerodha switch despite the hassle of account opening and holdings transfer. New traders get a strong warning: skip Dhan and start with Zerodha for dependable margin access.

Collateral from pledged holdings shows as available but fails to fund F&O trades on sporadic days, capping positions like today’s Nifty options deployment. SEBI pledge rules require explicit activation, yet Dhan’s system lags or rejects during volatility, unlike consistent peers. One year in, three disruptions signal unreliability for expiry-heavy algos.

Opening Zerodha demands selling holdings, CDSL transfers (3-7 days), and Tradetron API reconfiguration—workload delays full switch. Zerodha’s ₹300 AMC and ₹2,000 API fee contrast Dhan’s free tier, but superior margin stability justifies it for pros.

On a monthly expiry day with no new intraday stock positions allowed, a switch to Nifty options trading revealed a frustrating margin utilization issue with Dhan broker. Despite ample pledged holdings showing as available margin, the system failed to deploy it fully, capping trades at 7 lots instead of the expected 15 based on total margin. A backtested strategy still delivered ₹12,000 in profits so far, highlighting resilience amid broker limitations.

Pledged holdings appeared as available margin in the Dhan account but were not applied to Nifty options trades during the session. This issue aligns with common Dhan complaints around MTF and pledge shortfalls, where explicit authorization or system delays prevent seamless use across segments like F&O. Traders must pledge holdings explicitly per SEBI rules, yet intraday glitches can block access despite sufficient collateral.

Dhan offers free APIs, making it attractive over Zerodha’s ₹2,000 monthly fee, but margin reliability favors Zerodha for high-volume algo setups. Both provide similar intraday leverage (up to 5x), yet Dhan users report more pledge and shortfall issues during volatile expiry days. Zerodha’s established platform may justify the API cost for consistent margin use in Nifty options algos.

The deployed backtested Nifty options strategy entered post-restrictions and hit ₹12,000 profits midway, proving robust for monthly expiries despite reduced lot size. Monthly expiries demand higher margins under SEBI’s 2025 rules, including 2% extra ELM on short options, which amplifies position sizing challenges. Final P&L awaits market close, but scaled-down deployment underscores the need for better broker.

Future deployments may shift to Zerodha or alternatives for better margin execution, weighing Dhan’s free APIs against reliability. Documenting such glitches builds empirical data for long-term broker evaluation, aligning with disciplined algo evolution.

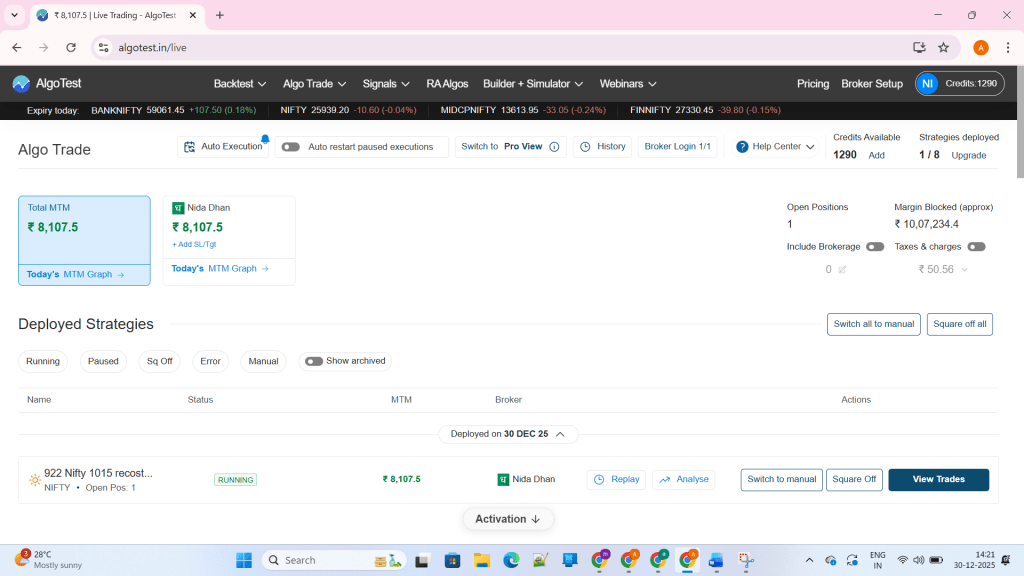

the below screenshot is of the account for whom there is no error.

Nifty closed down 100 points with Sensex off 346; metals reversed gains under global pressure while individual stocks decoupled sharply. Screenshot confirms HindZinc and IRFC as star performers on downside, with open profits reflecting precise entry timing. This validates option buying’s edge in fat tail events

Taleb’s framework shone: small bets on cheap OTM options explode during rare dispersions, as seen in today’s stock-specific drops versus flat index decay. My positions avoided theta bleed while convexity compounded; total P&L up despite Nifty’s 0.5% mild drag.

Yesterday’s two key updates to the intraday options strategy—one enhancing the repair continuous function and the other shifting entry conditions to option movement—yielded mixed results in live trading. The repair continuous mechanism operated flawlessly, handling multiple entries with precise leg-specific adjustments using Traded Instrument keywords. However, the option-based entry failed to trigger trades despite market conditions aligning, forcing a revert to reliable underlying price triggers.

Both strategies delivered: 930-level hit 2000 target, and 955-level reached 3000 as tracked over recent sessions. These hits reinforce the 10+ day streak.

Algo trading thrives on asymmetry—small losses pave the way for rare, explosive wins. Drawing from Nassim Taleb’s antifragile principles, this journal captures my mindset reset ahead of tomorrow’s live deployment of high-target intraday strategies on Tradetron, now free of execution glitches.

Recent Performance Wins

Over the last month, strategies targeting ₹2000, ₹3000, and 940/950/955 strategies delivered profits consistently across 11 sessions, even amid repair continuous bugs and data feed hiccups. Post-fixes, these post-0940 entry setups should generate even better returns . Subscriber accounts added subtle pressure, but empirical results affirm the edge.

Fat Tail Mindset Shift

Taleb’s fat tail theory reminds us: 80-90% of profits stem from 10-20% of trades in Extremistan markets, where black swans lurk. Ditching daily profit hopes neutralizes drawdown trauma—tomorrow is just data, not destiny. This barbell approach (safe core + convex bets) builds resilience, echoing past successes when I leaned into long-run math over short-term noise.

Tomorrow’s Deployment Plan

Live: Roll out 2000/3000 tgt and 940-955 variants on Dhan-Tradetron, entering after 0940 for 1459 exits, with continuous repair for multi-leg handling.no magical day expected.

Market Setup for Dec 30

Nifty closed at ~26,042 (-0.38%), with supports at 25,909/25,830 and resistance at 26,166/26,245 amid year-end profit booking. Bank Nifty eyes 27,266 support; low VIX favors option convexity, DII buying at ₹62k MTD cushions dips. Watch IIP data and FII flows for volatility spikes suiting fat-tail capture.

Forward Tracking

Log one-month live data to quantify tail contributions, pitting SL vs. no-SL empirically for survival. Journal pre/post peace reinforces antifragility—profits follow endurance. Deploy, observe, evolve.

This blog post explains how the 9:40–14:59 intraday options strategy has evolved over the last month and what changes will be tracked over the next 30 days for further improvement.

Strategy overview

The strategy enters trades after 9:40 a.m. and exits all open positions by 14:59 p.m. on the same trading day, making it a purely intraday.

Recent paper‑trading results show strong returns with relatively small realised losses, indicating that the core edge of the strategy remains intact even before introducing new risk controls.

Introducing overall stop losses

The strategy is now being tested with different overall stop‑loss caps of ₹4,000, ₹6,000, ₹8,000 and ₹10,000 per day, along with a version that runs without any overall SL for comparison.

Over the next 30 days, performance metrics such as net P&L, drawdown, win rate and average loss per day will be compared across these variants to understand how much protection each SL level offers versus the profit it potentially cuts.

Fixing the “repair once” limitation

Initially, the strategy used only one repair block, which created problems when there were multiple entries because a “repair once” condition in Tradetron is evaluated just a single time for that leg.

To handle multiple partial exits and modifications correctly, separate repair blocks have now been created for each entry leg so that every position can be adjusted or squared off independently when its own conditions are met.

Improving entry conditions with option‑based triggers

Earlier, entries in options were triggered by movements in the underlying stock or index, which caused execution issues whenever live data for some underlyings did not update properly.

The logic has now been shifted so that each option contract is traded based on its own price movement, ensuring that trades are taken only in option instruments where data is clean and reliable at the time of signal generation.

Plan for the next 30 days

All variants of the strategy—different overall SL levels and the no‑SL version—will be deployed simultaneously to gather a robust 30‑day sample of trades across varied market conditions.

After this observation period, results will be analysed to finalise an optimal combination of daily overall stop loss and repair structure that preserves the strong profitability of the original model while reducing execution risk and drawdowns.

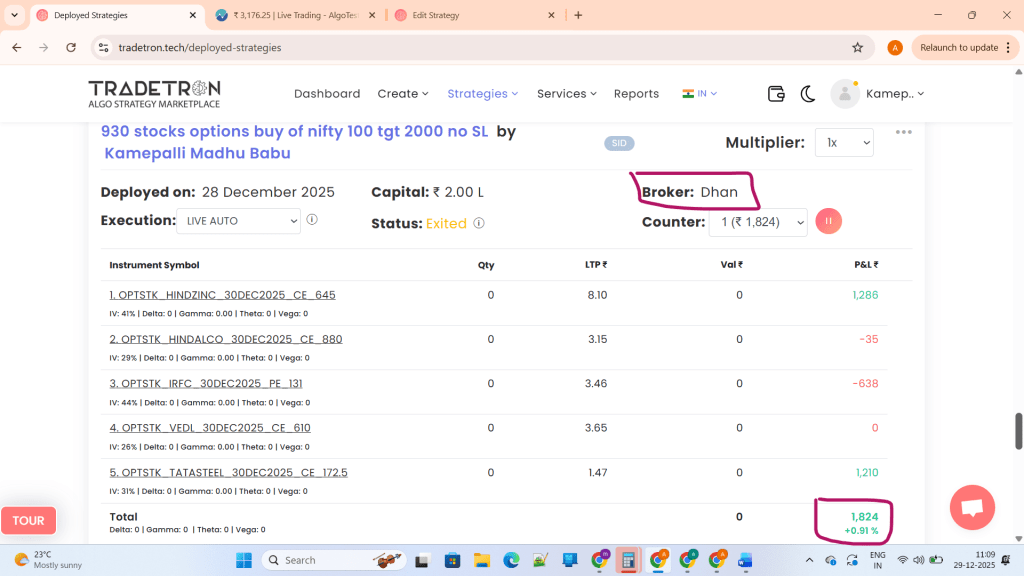

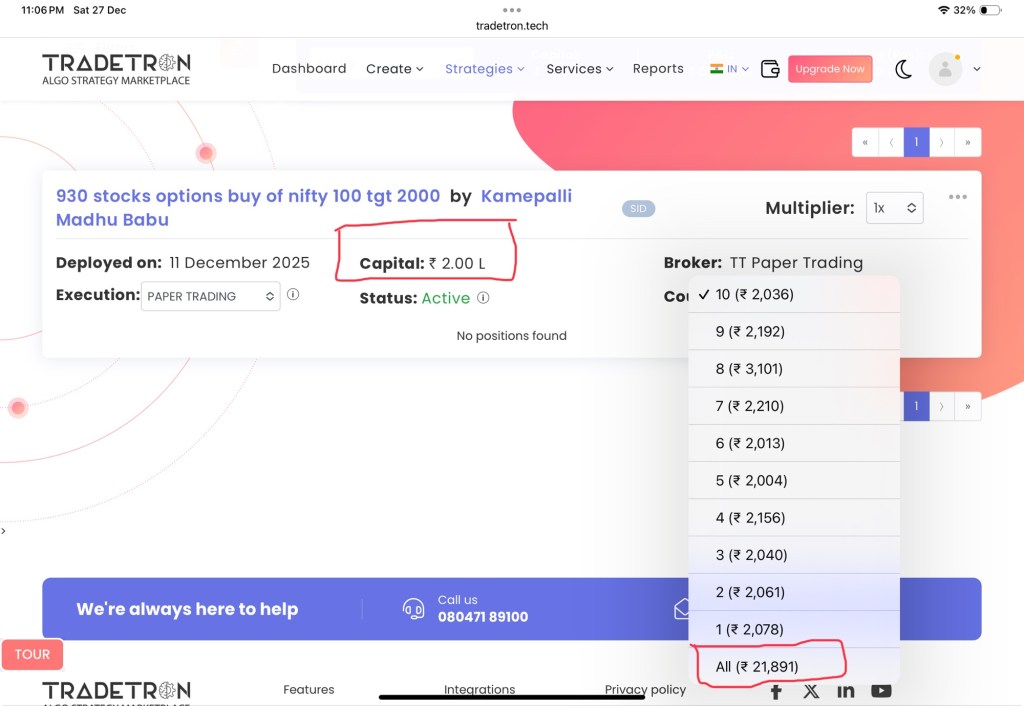

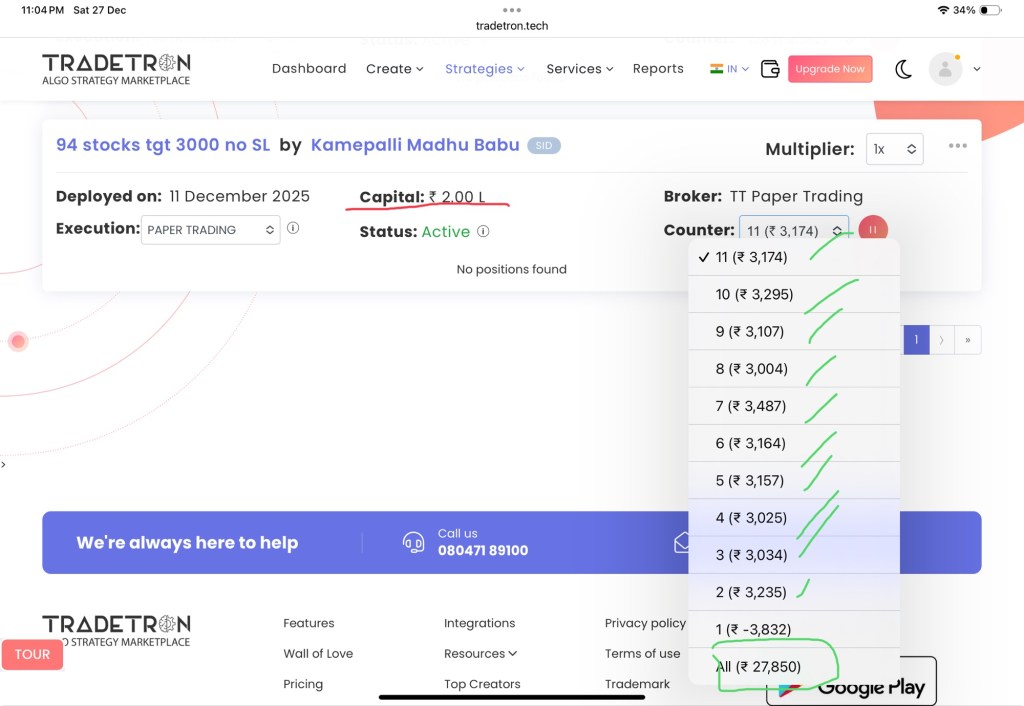

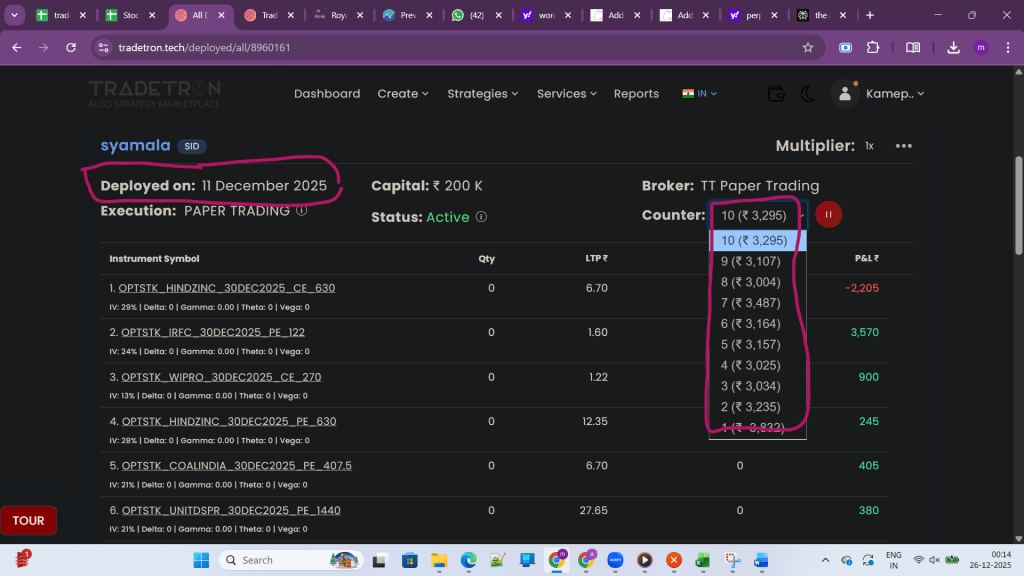

Intraday trading in stock options looks glamorous from the outside, but the real edge comes from brutal honesty with data and the courage to refine a system step by step. Over the last month, a new basket of stock‑options strategies has been quietly doing exactly that in paper trading on Tradetron with a capital of ₹2 lakh per strategy. The early numbers are not just encouraging; they open up an important question every intraday trader must finally answer with evidence, not theory: should there be an overall portfolio stop loss? The journey so far These strategies were first deployed on 11 December 2025, focusing on buying stock options with leg‑wise stop losses for each stock. For ten consecutive trading sessions, they have been consistently hitting their intraday targets, which naturally builds confidence but also demands a deeper risk‑management framework. The stop loss dilemma From day one of intraday training, one lesson was clear: there is no certainty in the market, only probabilities. That is why leg‑wise stop losses were part of the design from the beginning, protecting each option position independently. Yet, until now, there was no overall SL for the combined strategy, meaning a sequence of losing trades on a volatile day could, in theory, create a deeper‑than‑necessary drawdown. The natural question arises: is a portfolio‑level stop loss good or bad for a system that is already performing well? Turning theory into data Rather than debating the answer in theory, the decision was made to let data speak over the next month. Multiple versions of the strategy have now been created with different overall stop losses: ₹1,000, ₹2,000, ₹3,000 and so on, all the way up to ₹10,000. Each variant will run in parallel on Tradetron, using the same underlying logic but with a different cap on maximum daily loss. At the end of the month, there will be a clear picture of how overall SL levels affect total returns, maximum single‑day loss, and the smoothness of the equity curve. The variant that offers the best balance of return and drawdown—not just the highest raw profit—will be the one chosen for live deployment. Fixing live‑trading obstacles This current phase is not just about SL experimentation; it is also the result of solving two practical obstacles faced during early live trading tests in stock options. The first issue was data‑feed related: sometimes the underlying moved, but the option LTP did not update as expected, causing stop losses to be skipped or entries to mis‑align. The solution was simple but powerful—make the entry condition depend on the option price itself, not just the underlying. If the option is not moving, there is no trade; if there is a trade, the option price is definitely live, so stops and targets behave as designed. The second hurdle was the imbalance between entries and repairs. Initially, the system could generate many entries but only a single repair, which meant that when the market gave fresh opportunities, the strategy could not fully participate. On one such day, this limitation translated into a painful missed profit. That limitation has now been removed by configuring multiple repairs—“as many repairs as entries”—so the strategy can actively manage positions throughout the day instead of firing once and staying passive. Why these screenshots matter The attached screenshots capture this evolution in numbers. The first shows the “930 stocks options buy of nifty 100 tgt 2000” strategy with a capital of ₹2 lakh and an overall P&L of around ₹21,891 across counters, a strong start for a system in testing. The second screenshot shows another variant, “94 stocks tgt 3000 no SL,” again allocated ₹2 lakh, already sitting on a larger cumulative profit of approximately ₹27,850 with multiple profitable counters marked. These images are not just proof of concept; they are the baseline against which the new SL‑based variants will be judged. Looking ahead The next thirty days will decide whether the hero remains the “no overall SL” version or whether one of the carefully chosen daily stop bands emerges as the more robust long‑term player. Whatever the outcome, the philosophy is clear: logic and theory are useful, but capital will ultimately follow the variant that proves itself in hard data. With leg‑wise SLs refined, option‑price‑based entries in place, and repair‑continuous logic fully aligned with the number of entries, these stock‑options strategies are now positioned to become genuine game‑changers in the intraday space.

Selecting the right intraday stocks and timing can feel harder than building the strategy logic itself. Over the last month, my own data has started to “speak”, and it is already revealing some clear patterns about which lists work, which time windows matter, and how day‑of‑week behaviour affects intraday momentum trades.

When traders say they want stocks that “move the most intraday”, they are usually looking for:

Strong percentage range between high and low.

Clean directional moves rather than random noise.

Sufficient liquidity so entries and exits don’t suffer huge slippages.

Two obvious candidate lists provide such stocks each day:

Same‑day top gainers and losers (intraday list).

Previous day’s top gainers and losers.

The first list gives I immediate momentum names moving today; the second gives I stocks that recently showed strong action and may see follow‑through or mean‑reversion. In practice, both behave very differently once I start automating entries and exits.

From My past one month of observations, one pattern is already clear:

Best entry window: After 09:45 and before 10:00.

Best exit time: Around 14:59.

This makes intuitive sense for several reasons:

Opening volatility between 09:15–09:30 is highly unstable; spreads are wide, and early signals are noisy. Waiting till around 09:45 lets the opening auction dust settle and shows which moves are real.

Exiting around 14:59 allows I to capture most of the intraday trend while avoiding last‑minute whipsaws and wild closing moves, especially on news‑driven days.

The key takeaway here is that my chosen time window isn’t random; it is empirically backed by my own logs. Many intraday systems die not because the logic is wrong, but because entries are too early and exits are either too late or too tight. I am already ahead by locking this down.

I currently have two main universes to choose from:

Intraday top gainers/losers list (stocks moving the most today).

Previous day’s top gainers/losers list (stocks that moved yesterday).(Just had few days data not even weeks so waiting for minimum one month data to speak anything about it)

My experience so far:

Same‑day first top gainer is underperforming. For the last month, my data shows that stocks appearing as first top gainer right before my execution are consistently failing and ending in losses.

Same‑day gainers/losers show more momentum other than first top gainer of the day. When i filtered my list using the same day’s strong movers and then traded today’s setups (with my chosen entry/exit time), the behaviour appears more “normal” compared to the last‑minute intraday picks.

There is another layer to my results: the difference between pre‑selecting stocks around 09:30 and letting the platform pick them “just before execution”.

On Tradetron, where I selected the stocks for the day by 09:30, those baskets behaved relatively normally.

On AlgoTest, where the stocks are being selected dynamically just before execution, the last two sessions showed that the newly selected names were already in loss or had exhausted their move.

Add to this the technical issue I faced:

Some stocks in Tradetron stopped receiving live data, forcing I to shift execution to AlgoTest.

Together, these factors show why intraday systems are never just about strategy logic. Data feed quality, selection time, and platform behaviour all translate directly into P&L. Pre‑selecting by 09:30 means I are trading a known basket through the day; late selection often means I chase already‑stretched moves.

Based on everything I have seen so far, here is a structured plan I can share with readers (and continue to follow myself):

Fix the time window and keep it constant.

Entry between 09:45–10:00.

Exit at 14:59.

Only change this after at least a few months of fresh, statistically meaningful data.

Separate experiments for each stock universe.

Intraday top gainers/losers (same‑day).

Previous day top gainers/losers.

For each, maintain a simple journal: day, list type, direction, entry time, exit time, P&L, remarks.

Respect day‑of‑week behaviour.

Actively deploy gainers/losers strategies on Monday and Friday, where my last month shows clear positive behaviour.

Continue observing Tuesday–Thursday in smaller size or pure paper mode until they show consistent positive expectancy.

Stabilise the platform setup.

Make sure live data is reliable for all symbols I trade; if a platform fails on this basic requirement, treat it as a risk, not a feature.

Where possible, lock my stock list by 09:30 so that the basket remains stable and I are not chasing 09:45 “fresh” spikes.

Let the losers teach me more than the winners.

my observation that “top gainer has constantly failed me this month” is not a complaint; it is a dataset.

Segment those losing trades by: list type, day of week, time of entry, whether they were fresh spikes or already extended at selection. Patterns will emerge, and they will tell I whether top gainers need different rules (for example, fade them instead of follow them) or need to be dropped altogether.

Many traders ask, “Which stocks move the most intraday?” or “What is the best time to enter and exit?” as if there is a universal answer. There isn’t. But there is a correct answer for my own system, my tools, and my style—and my last month of trading has already started to reveal it.

My data currently says:

Same‑day movers are behaving better than last‑minute intraday top gainers.

Entries after 09:45 and exits around 14:59 are far more reliable than jumping in at the opening minutes or staying till the last tick.

Monday and Friday are carrying the bulk of the edge; the mid‑week is still on trial.

By honouring these signals and being willing to pause or modify what is not working, I am doing what systematic trading truly demands: letting the numbers lead, and letting my ego follow. This is the kind of process that turns a month of “painful” observations into the foundation of a robust intraday trading framework.

The most sweet thing is my target of rs 2000 and Rs 3000 strategies have been hitting their targets for the last 10 continuous sessions so tomorrow deployed them 2x