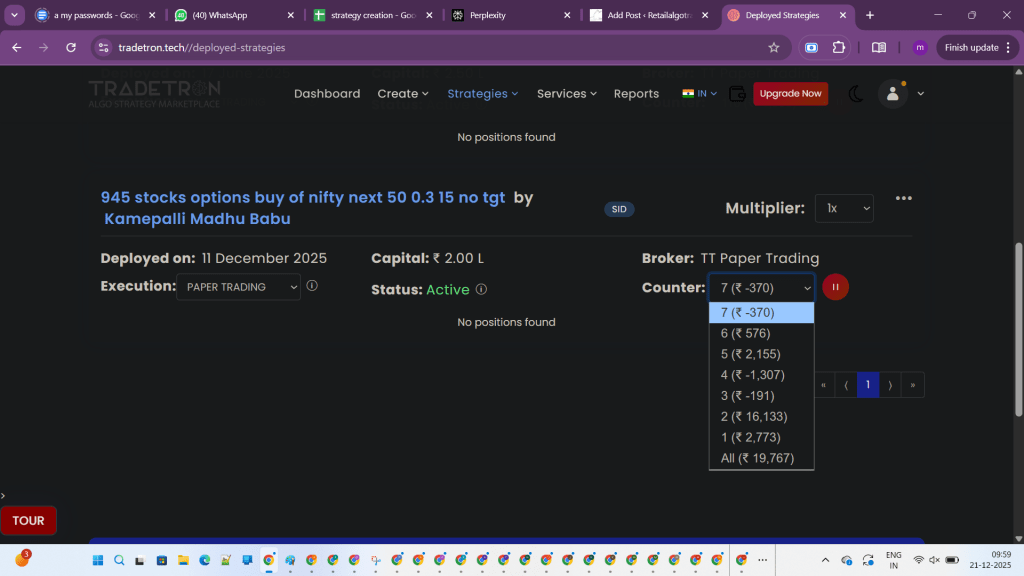

On a monthly expiry day with no new intraday stock positions allowed, a switch to Nifty options trading revealed a frustrating margin utilization issue with Dhan broker. Despite ample pledged holdings showing as available margin, the system failed to deploy it fully, capping trades at 7 lots instead of the expected 15 based on total margin. A backtested strategy still delivered ₹12,000 in profits so far, highlighting resilience amid broker limitations.

Pledged Holdings Margin Not Utilized

Pledged holdings appeared as available margin in the Dhan account but were not applied to Nifty options trades during the session. This issue aligns with common Dhan complaints around MTF and pledge shortfalls, where explicit authorization or system delays prevent seamless use across segments like F&O. Traders must pledge holdings explicitly per SEBI rules, yet intraday glitches can block access despite sufficient collateral.

Dhan vs Zerodha for Algo Trading

Dhan offers free APIs, making it attractive over Zerodha’s ₹2,000 monthly fee, but margin reliability favors Zerodha for high-volume algo setups. Both provide similar intraday leverage (up to 5x), yet Dhan users report more pledge and shortfall issues during volatile expiry days. Zerodha’s established platform may justify the API cost for consistent margin use in Nifty options algos.

Strategy Performance on Expiry Day

The deployed backtested Nifty options strategy entered post-restrictions and hit ₹12,000 profits midway, proving robust for monthly expiries despite reduced lot size. Monthly expiries demand higher margins under SEBI’s 2025 rules, including 2% extra ELM on short options, which amplifies position sizing challenges. Final P&L awaits market close, but scaled-down deployment underscores the need for better broker.

Future deployments may shift to Zerodha or alternatives for better margin execution, weighing Dhan’s free APIs against reliability. Documenting such glitches builds empirical data for long-term broker evaluation, aligning with disciplined algo evolution.

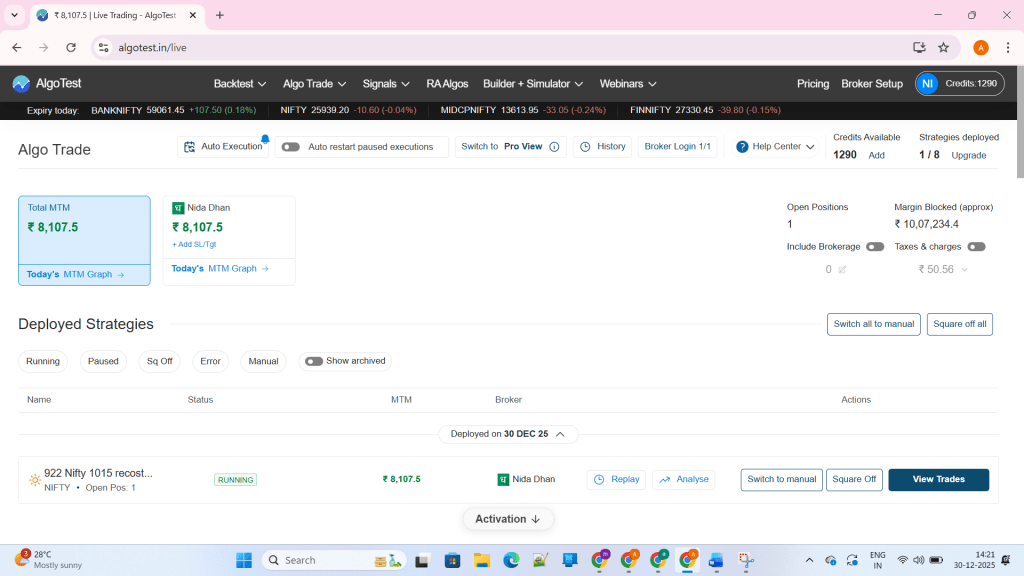

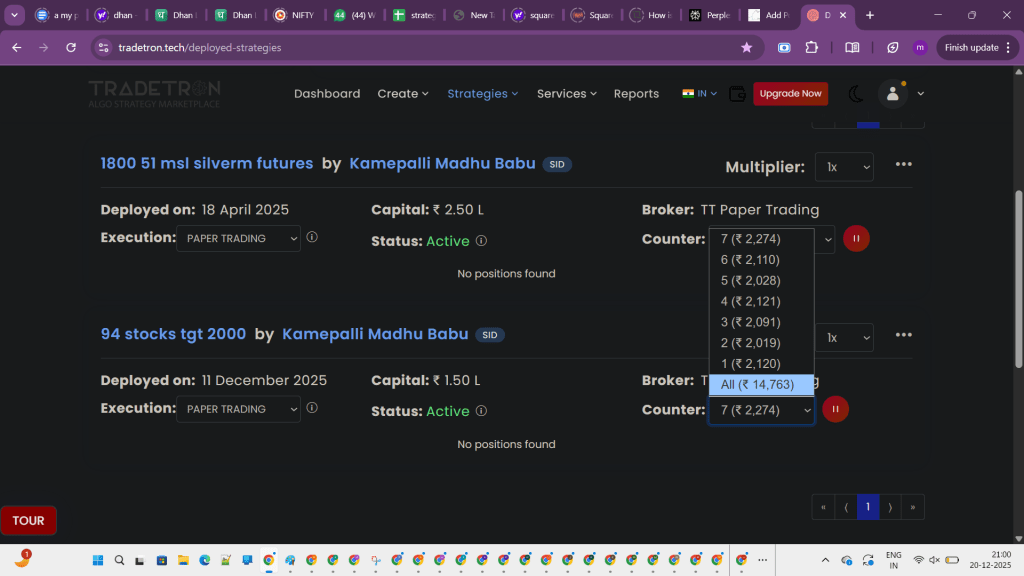

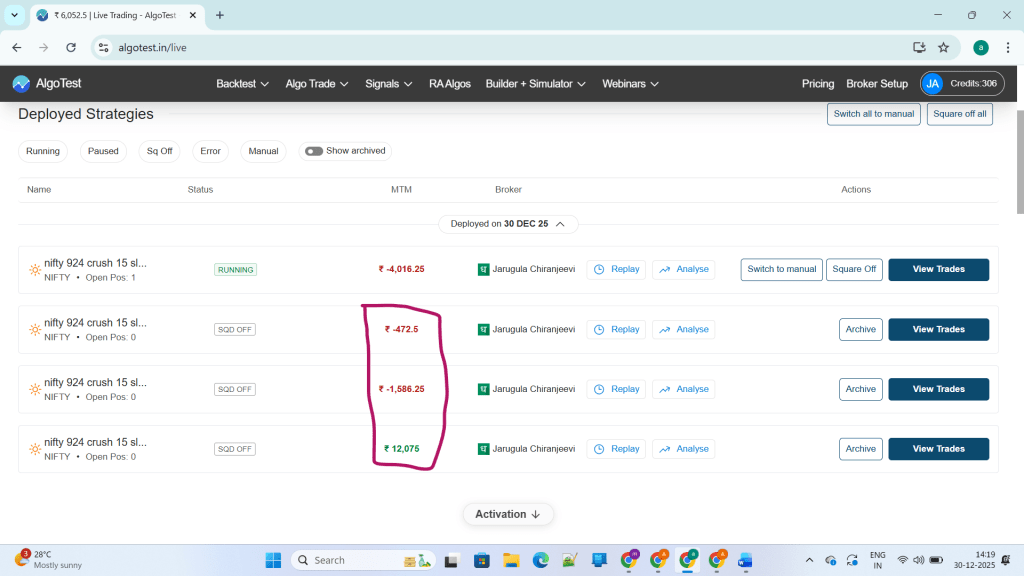

the below screenshot is of the account for whom there is no error.