This blog post explains how the 9:40–14:59 intraday options strategy has evolved over the last month and what changes will be tracked over the next 30 days for further improvement.

Strategy overview

- The strategy enters trades after 9:40 a.m. and exits all open positions by 14:59 p.m. on the same trading day, making it a purely intraday.

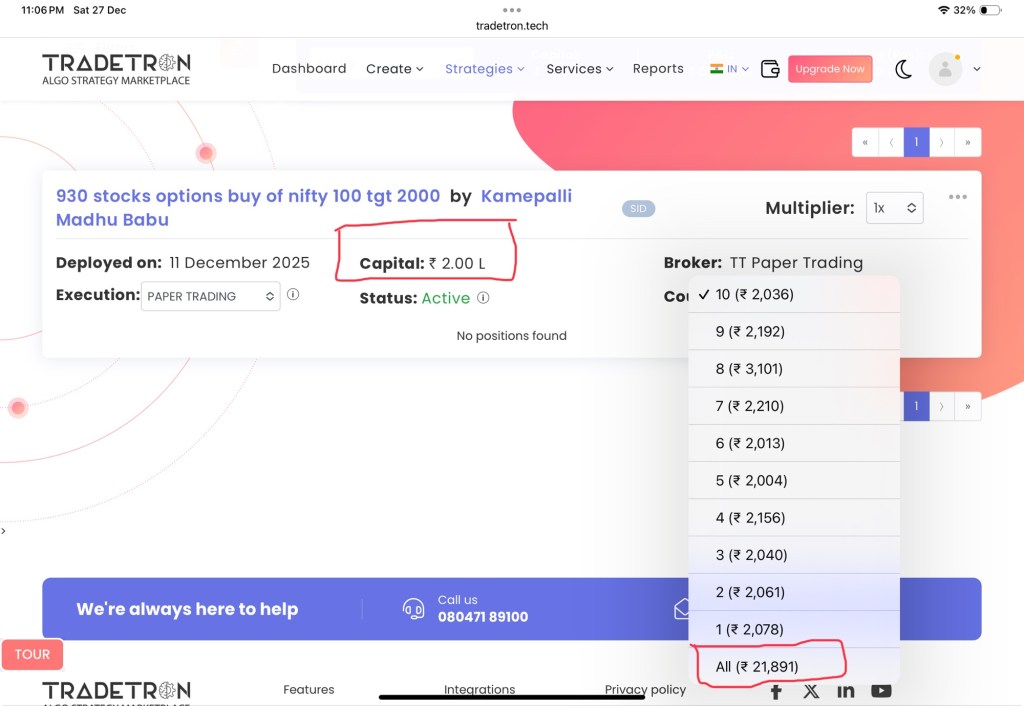

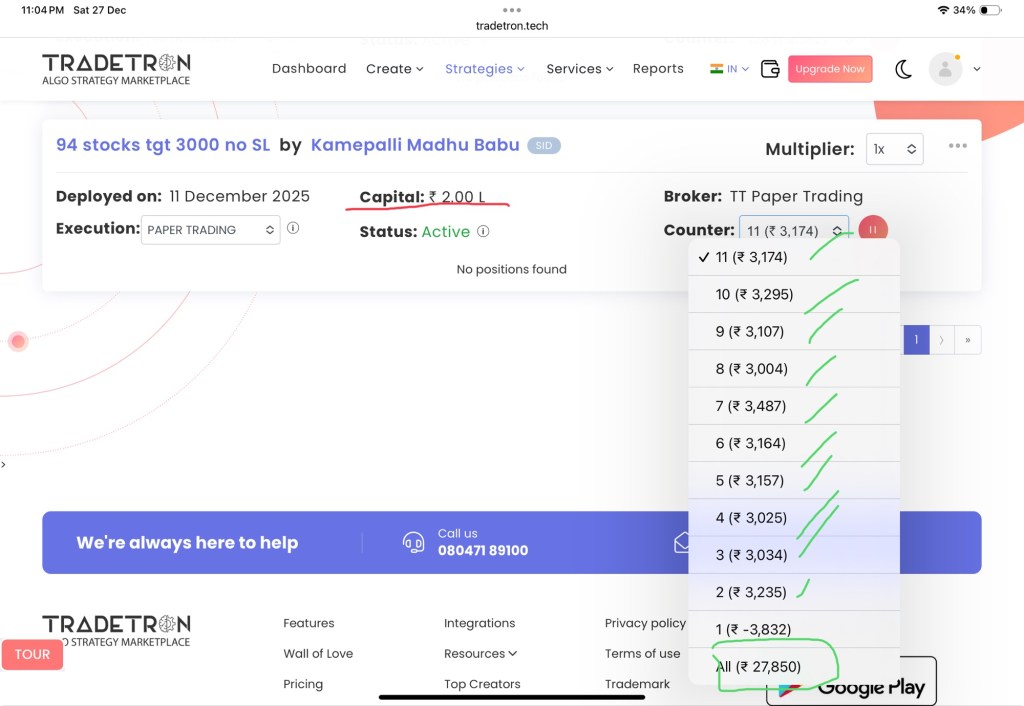

- Recent paper‑trading results show strong returns with relatively small realised losses, indicating that the core edge of the strategy remains intact even before introducing new risk controls.

Introducing overall stop losses

- The strategy is now being tested with different overall stop‑loss caps of ₹4,000, ₹6,000, ₹8,000 and ₹10,000 per day, along with a version that runs without any overall SL for comparison.

- Over the next 30 days, performance metrics such as net P&L, drawdown, win rate and average loss per day will be compared across these variants to understand how much protection each SL level offers versus the profit it potentially cuts.

Fixing the “repair once” limitation

- Initially, the strategy used only one repair block, which created problems when there were multiple entries because a “repair once” condition in Tradetron is evaluated just a single time for that leg.

- To handle multiple partial exits and modifications correctly, separate repair blocks have now been created for each entry leg so that every position can be adjusted or squared off independently when its own conditions are met.

Improving entry conditions with option‑based triggers

- Earlier, entries in options were triggered by movements in the underlying stock or index, which caused execution issues whenever live data for some underlyings did not update properly.

- The logic has now been shifted so that each option contract is traded based on its own price movement, ensuring that trades are taken only in option instruments where data is clean and reliable at the time of signal generation.

Plan for the next 30 days

- All variants of the strategy—different overall SL levels and the no‑SL version—will be deployed simultaneously to gather a robust 30‑day sample of trades across varied market conditions.

- After this observation period, results will be analysed to finalise an optimal combination of daily overall stop loss and repair structure that preserves the strong profitability of the original model while reducing execution risk and drawdowns.