In algorithmic trading, consistency matters far more than occasional big wins. Anyone can show one good day. Very few can show daily discipline, controlled risk, and repeatable outcomes.

Today, I want to share one such strategy—simple in concept, powerful in execution.

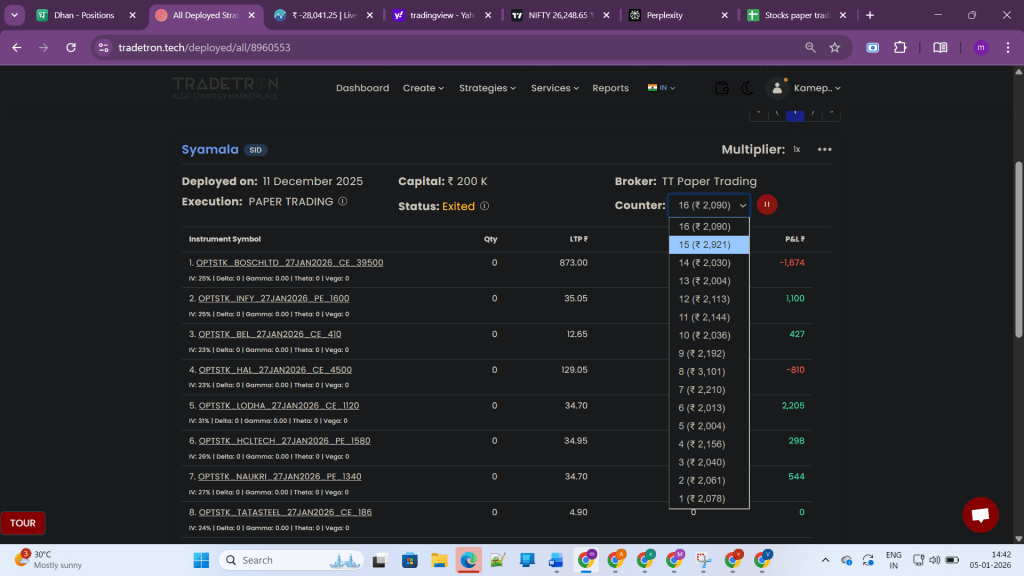

🎯 Daily Target: ₹3,000

📈 And It Has Been Hitting—Day After Day

This 30 Stocks Options Buy Strategy is designed with a clear objective:

- Small, achievable daily target

- Strict risk management

- Broad diversification across stocks

- No over-optimization, no over-trading

And the results speak for themselves.

➡️ Daily target of ₹3,000 has been consistently achieved, making it a strategy built for sustainable returns, not adrenaline trading.

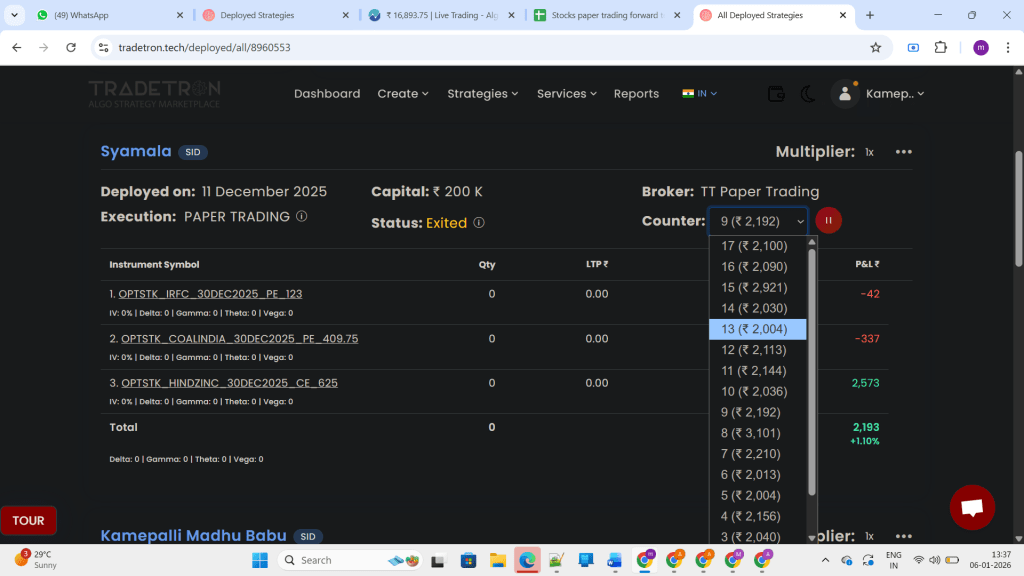

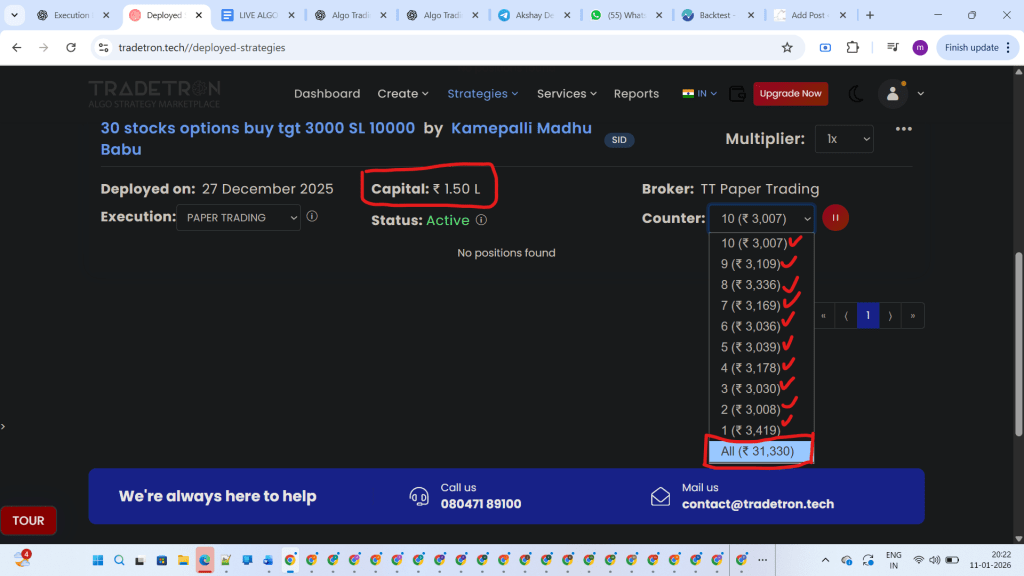

💼 Capital Efficient & Scalable

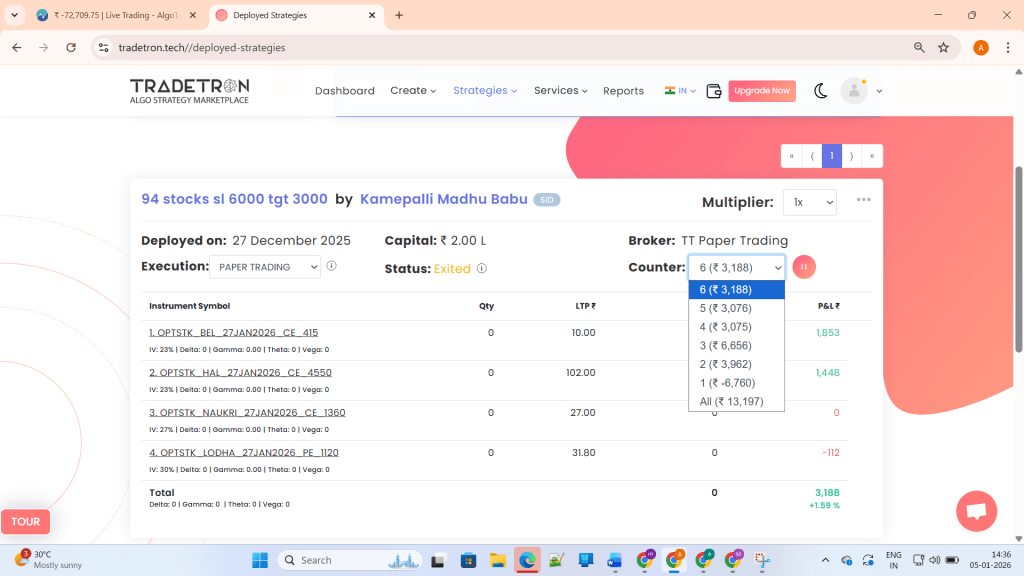

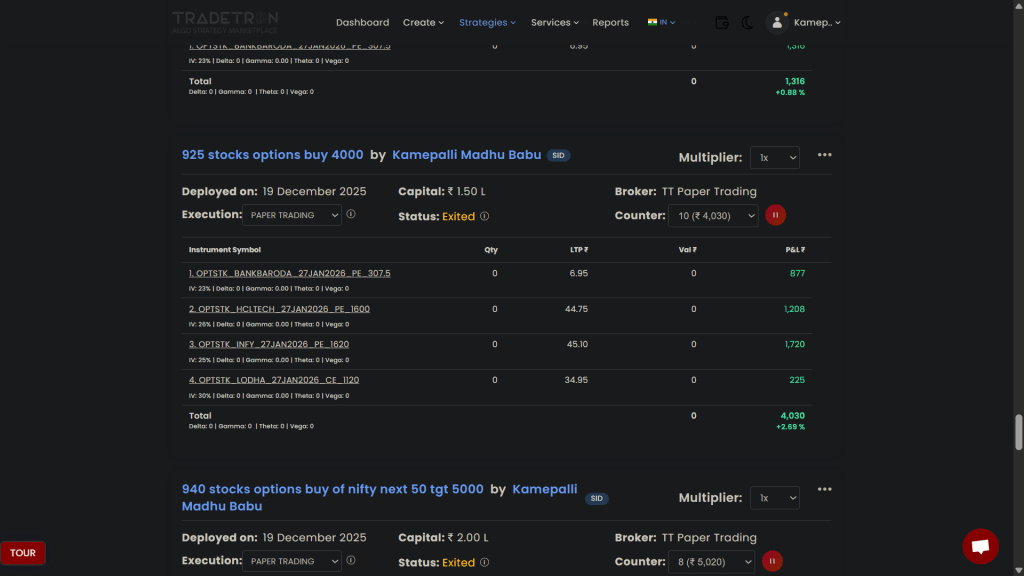

- Deployed Capital: ₹1.50 Lakhs

- Per-Stock Target: ~₹3,000

- Execution Mode: Live & Paper (tested thoroughly)

This makes the strategy:

- Beginner-friendly

- Capital-efficient

- Easily scalable using multipliers

Whether you’re starting small or planning to scale systematically, this strategy fits well into a disciplined trading framework.

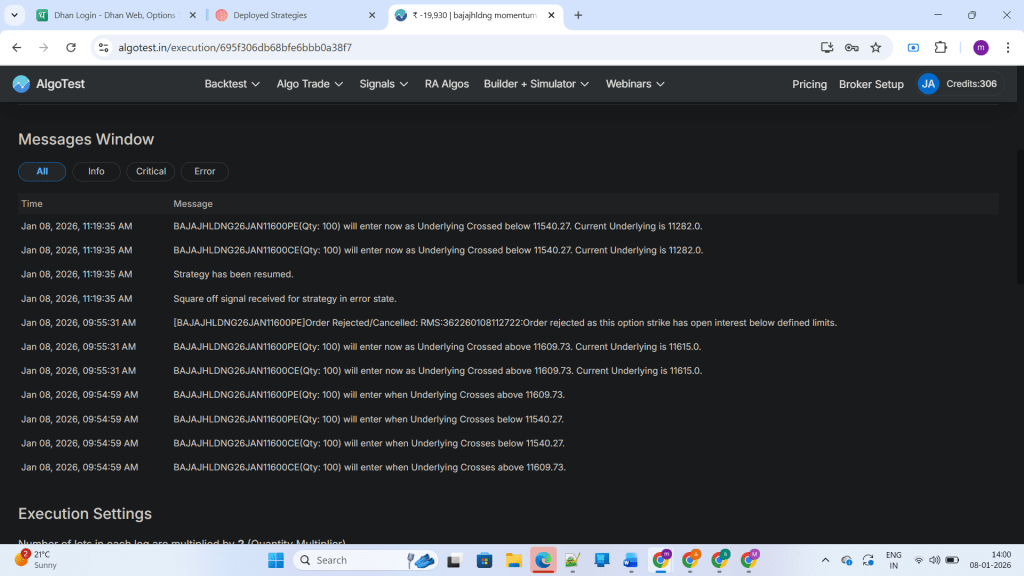

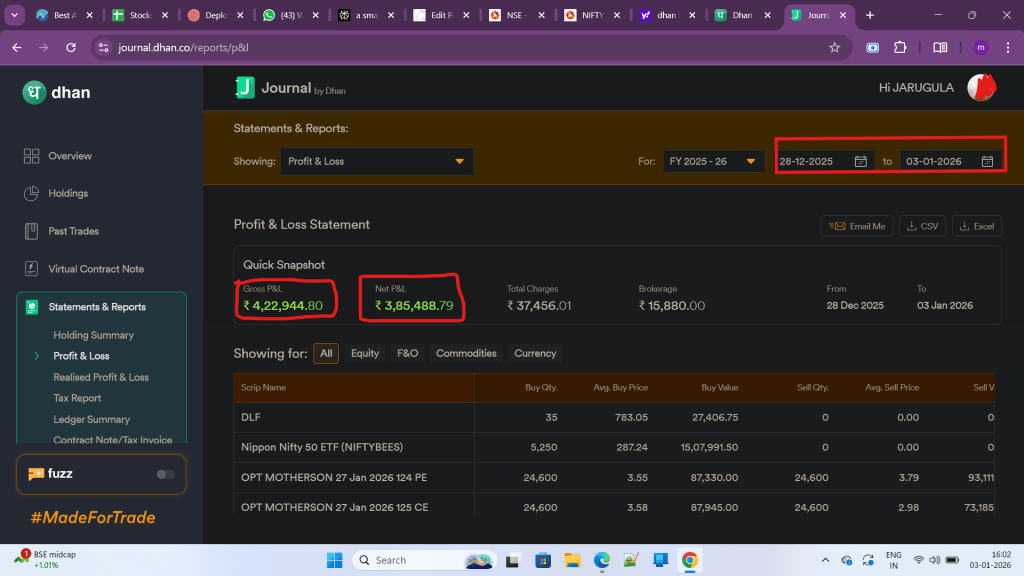

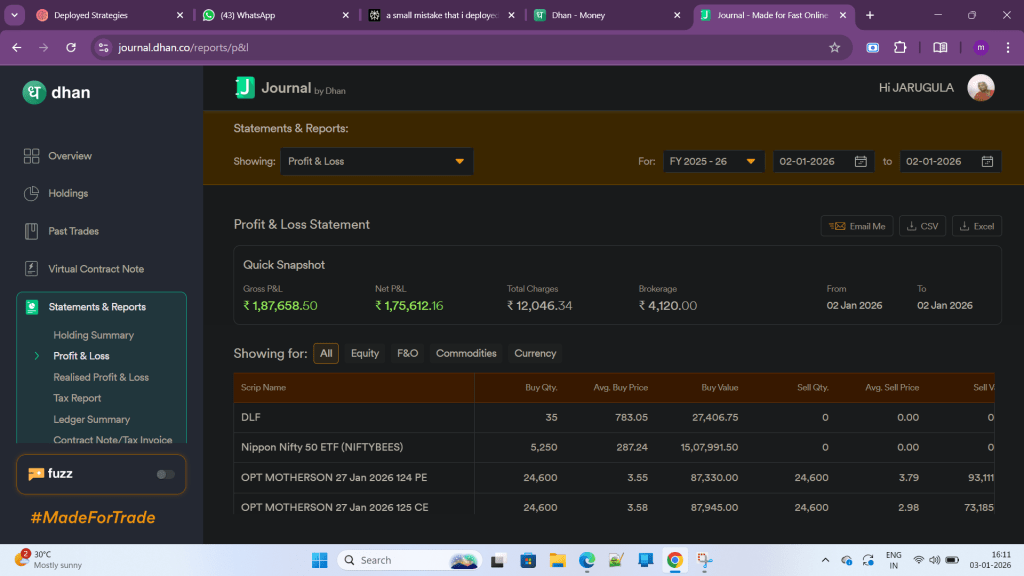

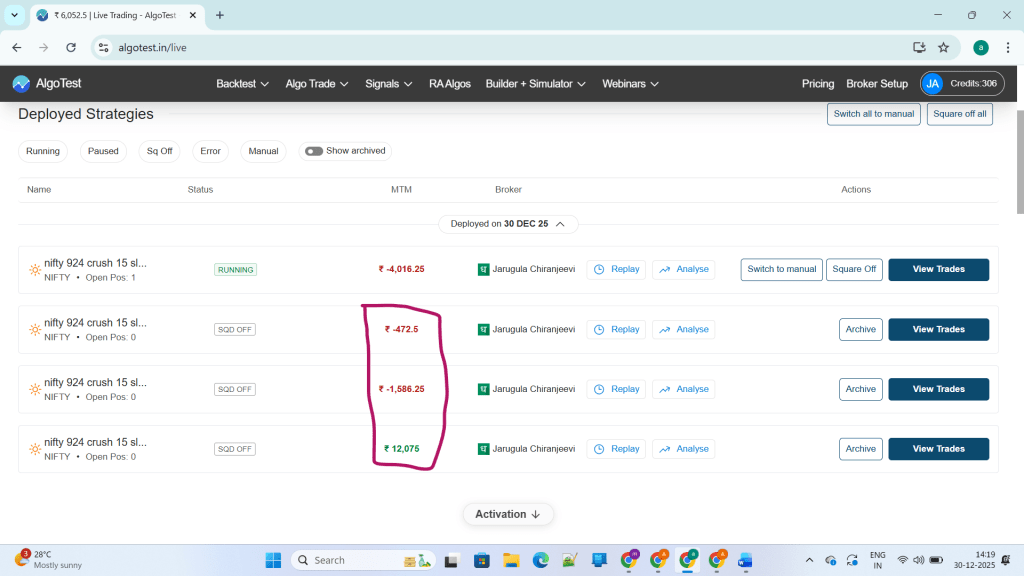

🔴 Live Deployed – Not Just Backtested

This is not a theoretical setup or a cherry-picked backtest.

✅ The strategy is deployed LIVE

✅ Trades real market conditions

✅ Faces real volatility, RMS checks, and execution realities

Transparency is non-negotiable.

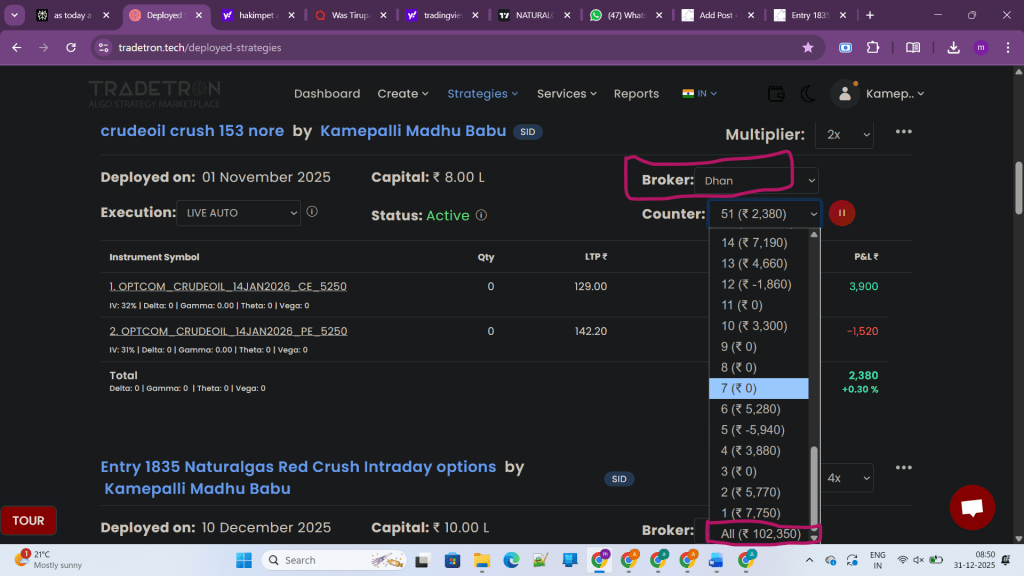

🔗 Strategy Details (For Serious Traders)

- Strategy Name: 30 Stocks Options Buy – Target 3000

- Strategy Link:

👉 https://tradetron.tech/strategy/9039145 - https://tradetron.tech/strategy/9039145

- Live Shared Code:

🔐9c8077a4-ead6-4258-9ed6-043f86ecf379

You can verify, observe, and track the strategy yourself.

🧠 Why This Strategy Works

What makes this strategy stand out is not aggression—but structure:

✔ Diversification across 8 stocks

✔ Defined target & stop-loss

✔ No dependency on market direction

✔ Designed for calm, rule-based execution

✔ Minimal emotional interference

This is the kind of strategy meant for traders who value peace of mind as much as profits.

📌 For Whom Is This Strategy Ideal?

This strategy is suitable for:

- Traders tired of over-trading

- Working professionals seeking passive algo income

- Traders who prefer steady daily targets

- Subscribers who value process over hype

If your goal is to grow capital slowly, steadily, and responsibly, this strategy deserves your attention.

🚀 Final Thoughts

Markets reward discipline, not excitement.

This strategy doesn’t shout.

It doesn’t gamble.

It simply shows up every day and does its job.

If you’re looking to align with a tested, live-deployed, transparent algo strategy, you’re welcome to explore it using the shared link and code above.

📊 Consistency compounds.

📈 Discipline delivers.

— Kamepalli Madhu Babu

Algo Trader | Strategy Designer |